|

Hi Heather!

I'm 22 years old and I've been trying to get a good control of my finances. I'm still a student so I don't have a regular income. I've set up a LISA account to save for a house but I'd also like to begin saving for retirement. I've looked everywhere online but nothing seems to explain what different kinds of pensions there are, how to open them and how they work. Please help! Alex

Alex, this is an amazing question to be coming from a 22 year old! Well done for setting up a Lifetime ISA, that's a good move especially as they are considering phasing that scheme out.

I have been meaning to write a post on personal pensions this since Christmas because another person asked a few specific questions so I’ll tick their questions off in this post too as they could apply to you as well at some point in the future. PENSIONS! Pensions are one of my favourite topics. If you were in a job you would have access to either:

What you need to open is a self-invested pension plan or SIPP. When you do have a work place pension, you can also have a SIPP in addition to it; there are no penalties for doing so unless you’ve reached the annual limit for investing in a pension but this isn’t something most people need to worry about. Once you open a pension account, you need to decide how you want your money to be invested. This is your decision unless you hire a financial adviser. However, even if you do get financial advice I always strongly advise getting some financial knowledge so that you can judge whether you agree with the advice you are getting or not. Every financial adviser has her own beliefs and biases about investing, that's human, the question is whether you agree with her. Most people don’t know a lot about investing (including me when I started working) so some investment sites might ask you to answer a few questions on how you feel about risk-taking and then they suggest “ready made portfolios” to you to invest in which would be aligned with what you say your risk tolerance is, your “stated” tolerance for risk. On some sites you might have access to “target retirement funds” this means you state when you want to retire and they adjust the risk of your investments based on that. For example, if you want to retire at the age of 62 which is 40 years from now, in your case, you would select a 2060 target retirement portfolio. The fund manager would then manage the risk by investing in more risky stuff now when you are far away from retirement and as you approach retirement the balance of investments would be adjusted away from higher risk, higher return investments towards lower risk, lower return investments. The risk-return relationship is very important here. If you say you have a lower tolerance for risk then the options you will be given will have a lower associated risk but also a lower return on your money. If you have a long time until retirement, and being 22 Alex, you have a very very long time until you need to retire then you can afford to take more risk. Personally, 100% of my stock investments are in equities (that is, they’re invested in company shares) because I get a fixed bond-like return from property investing so that balances it out. By comparison, the average investor will usually have a portion invested in bonds and a portion in equities. By buying bonds you lend money to companies or a government and they pay you a fixed amount for that loan. As a lender, you are not a part-owner of the company and as such you don’t get a share of the company’s profits as you would if you invested in the shares. By the way: shares, stocks, equities are usually used interchangeably – they mean the same thing in most cases. Equities vs. bonds I won’t go into too much detail on equities vs. bonds but here are some important differences:

Why am I telling you all this? Because you need this sort of high level knowledge to decide how your money will be invested. What portion of your investments will you put into equities and what portion into bonds?

If you’re investing in ready-made portfolios and they give you an indication of risk, the higher risk portfolios have more equities and the lower risk portfolios have less equity investments. Single stocks or index funds You can manage your risk by only investing in funds or portfolios that invest in a wide variety of companies. Some people find it more exciting to buy a single company's shares (single stocks) but that is much more risky than investing in funds because a fund is a diverse portfolio of lots of companies. As Index funds include a large number of companies, the complete failure of any one of those companies would have a much more limited impact on your return. I have dabbled in buying single stocks myself and I can tell you that it’s very difficult to choose winning stocks – to maximise your chance of winning “buy a whole stock market”, either by buying index funds that track a whole country or by buying index funds that track a whole industry. If you do want to dabble in single stock investing, don’t put any more than 10% of your portfolio into them and as your portfolio gets larger I would reduce that to 5%. So, for every £1,000 invested don’t put more than £100 into single companies and as you move towards a portfolio worth £100,000 I would personally reduce single stocks to no more than 5% of my investments. These are arbitrary percentages and as you gain experience you will decide what feels more appropriate for you. Actively managed vs. passively managed funds There are two main types of fund to choose between, actively managed funds and passively managed funds. Passively managed funds track a whole market such as the S&P500 which tracks the 500 largest, listed companies in the US or the FTSE100 which tracks the 100 largest listed companies in the UK - I emphasise listed because there may be companies that are just as large as those listed on the stock market but because they are privately owned you wouldn’t have access to buy their shares. Alternatively, instead of tracking the whole market in a given country you can choose to invest in a specific sector such as utilities or technology or consumer goods. Actively managed funds have an actual person choosing which shares are likely to outperform the market and investing in such undervalued shares or choosing companies that are likely to grow rapidly and enjoy a rapid increase in value. The objective of an active manager is to beat the market index, while the objective of a passive fund is to match the return on an index. Now, you would think active funds, managed by "clever" fund managers are likely to beat the average market return from passive funds, right? Unfortunately, history has taught us that this very simply isn’t so: over 95% of the time fund managers do not beat index trackers. Not only that, the fees on actively managed funds are higher so even if you observe that an actively managed fund has achieved the same gross return as a market tracker you would be earning less from the active fund after fees have been deducted. Where to start? Where to start? I realise that this is all very technical stuff especially if you are beginner so here are links to a few indices to get you researching and investing. These are all funds I am invested in but I am not recommending you invest in them, only that you look at them to see what is included in each fund, what countries are represented, which companies are invested in, what the fees are and what returns have looked like over the last 5 years. I have put the fees each fund charges in brackets as the fees charged is one of the primary reasons I choose whether or not to invest in a fund. Fees can dramatically erode your return so you should always consider what the fees are before you invest in anything:

Even from the above you can see the large difference in fees between my actively managed fund and the passively managed ones. However, I am personally convinced by the management of Fundsmith. Their investment philosophies are aligned with mine and I think they have the potential to beat the market over time but I don’t put all my eggs into the Fundsmith basket despite my confidence in them. In summary, if you invest in a self-invested pension plan there is no commitment to a fixed pension income at the point of retirement. You therefore need to carefully decide how the money is invested. In doing this you need to consider:

Where can you open a SIPP? The biggest difference between the various platforms where you can open a SIPP is the user interface, customer service and the FEES. In a nutshell you might be charged any and all of the following fees:

Here are a few places you can open a SIPP account including the fees. The money to the masses website has a table showing what the fees look like depending on the amount invested. I recommend you have a look at that but below I share four that I consider to be popular and cost effective. Halifax share dealing

Hargreaves Lansdown

iWeb

Vanguard

Having only Vanguard’s funds is not necessarily a bad thing, they are cost effective and if you have an ISA elsewhere in addition to the SIPP at Vanguard, you can use that to invest in funds run by other institutions, e.g. Legal and General and Fidelity to name a few. Vanguard are very well rated in terms of performance and customer service in addition to having good fees. That said, you could save money on the account fee by investing in Vanguard funds via Halifax share dealing or iWeb and those two platforms would give you access to a wider variety of funds as well. Also, Vanguard’s minimum investment is £100/month or £500 lump sum. If you want to start out with £25/month which at your age is absolutely fine, then you need a platform that will allow lower monthly contributions. Where do I invest? I have a SIPP for my son at Hargreaves Lansdowne and I have a SIPP for myself at iWeb. The fees at iWeb were the cheapest for my ISA and I decided to have my SIPP there too as the fees were reasonable although not the cheapest at the time I opened it. It didn’t make sense to have a SIPP elsewhere to save not very much money. iWeb don’t offer junior ISAs and I wanted to keep my son’s SIPP with his ISA as well so I added it to his Hargreaves Lansdowne account. Based on the small amounts being added to his SIPP (£100 per month) the SIPP fees were actually cheaper at HL but they would have been more expensive for me because my SIPP account has much more invested than my son’s. To cut a long story short, where you choose to open a SIPP can also be influenced by where you have an ISA and whether you want these to be kept together. It’s not necessary to have your investments all in one place, I certainly have several investment accounts for various reasons. Before you decide speak to a few people including family members so you have a flavour for where your social circle seem to be investing, if at all. How much can you put into the SIPP each year? You can have a SIPP if you're resident in the UK whether or not you pay tax but your earnings impact the maximum amount you can put in each year. If you are not employed via the PAYE system, the maximum is £2,880 if you are not employed which becomes £3,600 including the government top-up which is equal to what you putting times 100/80. When you are employed you can put the equivalent of your full salary into your pension up to a maximum of £40,000 per year. I won’t go into lifetime limits for you as you are so young and will discuss those in my general post on pensions. Can you have a SIPP if you are a British citizen living abroad? You cannot make contributions to a SIPP if you are not a UK resident even if you have a British passport. You have to be a UK resident. If you have spent some of the year abroad and some of the year working in the UK, HMRC counts the number of days spent in the UK to confirm if you are UK resident. I won’t go into detail here because the actual number you need to qualify as a UK resident depends on whether you were a UK resident in the previous few years. You can, however, set up a SIPP if you're resident overseas and want to transfer a UK pension from a previous job to the SIPP (but you cannot make further contributions to it). So, for example, if you have a pension with a UK employer and want to transfer that to a SIPP while you are abroad, you can do that. If you’re resident abroad but paid in the UK and pay tax here you can also have a SIPP. So, for example, some British expats work abroad but are paid in the UK and pay a portion of their tax in the UK and are likely to qualify, however, speak to an accountant or financial planner to make sure you don’t fall foul of any rules if you’re ever in this complex domicile situation. What happens if the company you have your SIPP with goes bust? If your SIPP provider becomes bankrupt, your money should remain unaffected. Your money is not invested in the SIPP provider themselves; they either simply manage your investment or act as a platform for you to manage your own investments. I hope this helps! Heather References: What happens if my SIPP provider goes bust? Build a low-cost DIY pension Have a money question for me?

If you have any personal finance questions send them to [ME] – I will answer whatever piques my fancy via a blog post.

3 Comments

Hi Heather,

Thank you so much for launching your podcast. I am really enjoying all your advice. My name’s Vivienne. I’m single and in my late 60s. I receive the state pension and find that I struggle to make ends meet – my saving grace is that I own my home outright but I don’t have any other investments outside of that. Although I would like to work because I get lonely sometimes, I lack the energy I used to have in my younger days and certainly I find a full day’s work very exhausting nowadays. Is there anything you can think of that can help me boost my income? Thanks

Thanks for this question Vivienne.

Given you are not working, I won’t give you advice about saving and investing at this stage as I normally would. I’m sorry you get lonely – loneliness is a rising issue in Britain and not only amongst older people – in 2016/17 Younger adults aged 16 to 24 years reported feeling lonely more often than those in older age groups according to the Office of National Statistics. I have two income boosting suggestions for you that could help boost your income and reduce your loneliness too. In the past, I have also given people advice about boosting their income by monetising any skills they might have on freelance sites like fiverr.com or upwork.com or by tutoring via websites like tutorful. However, I am going to suggest something totally different to you, perhaps even radical: have you considered taking in a lodger or renting out any spare rooms you might have on airbnb.com? You could do this even if you didn’t own your home as long as you get permission from your landlord to sublet. There are pros and cons with each option. Option 1: LODGER If you take in a lodger, you will have someone living in your home on a full time basis and you will probably have to give up some of your space in places like the kitchen to them. You will also need to be comfortable with that person using your appliances and white goods. Are you happy for someone to share your hob, your fridge space, your washing machine and your living space that closely. Taking a lodger in could flip you from being lonely to being frustrated very quickly if that person has very different habits and a very different lifestyle to you. Instead of a full-time professional lodger perhaps you could take in a more transient lodger like a student. Some students, especially international students don’t see university as one long party and may well be studious, well-behaved and easy to live with. If the person comes from Europe, they are also likely to go back home regularly leaving you to enjoy your living space on your own terms during such periods. The government allows you to earn up to £7,500 a year tax free by letting a room in your home. This amounts to £625/month, all tax free. Given that the state pension currently sits at c.£8,800 a year, you would almost be doubling your income if achieved this amount. If you have a generous spare room with an ensuite you might well be able to charge this kind of rent. Or if you have two spare rooms you can get a couple of lodgers. You could also exclusively look for someone that is retired with the objective of keeping each other company in retirement. The type of person you decide to let a room to is entirely up to you. One downside is that you might find a lodger who keeps too much to themselves and isn’t interested in bonding with you which might make you feel even more lonely. This brings me to option 2. Option 2: AirBnB Have you considered renting any spare rooms out on AirBnB? If you have the energy to change sheets and provide a breakfast this can be a fantastic little earner especially if you live in a popular city. However, even if you are in a quieter city it is certainly something that is well worth trying. A major advantage of letting rooms out on AirBnB is that you will retain full control over your home and kitchen space. When you are not home, for instance, if you are on holiday or visiting friends and family you won’t be leaving the house to a lodger which may offer you some peace of mind. Just as importantly, during times when you expect visitors such as at Christmas you can have the house free of AirBnB guests. A key advantage of AirBnb over a lodger is that you will get exposure to many different types of people with many curious about you and your city – based on them having to rent an AirBnB you can assume that most won’t be as familiar with your local area as you are and you can enjoy telling them about it and where to visit. Personally, if I were in your shoes, I think I would go for the AirBnB option but you should decide based on your own personality and preferences. For instance, you might find the perfect lodger for you – someone who is perhaps older and not transient and even wants to spend time with you. When I was single, once I bought a house, I always had a lodger for two reasons: firstly, I didn’t like the person I was becoming when I lived alone – I was becoming very rigid and set in my ways; secondly, I needed the extra money because my first mortgage was expensive and the monthly income boost made a big difference to me. I was also very likely to always find lodgers that I had things in common with so we could do some things together. Just as with getting a lodger, you can rent rooms out on AirBnB and not have to pay tax until you are earning over £7,500. I hope this is helpful. Outside of this there are the more obvious things like getting a part-time job or baby sitting when you have the energy and inclination to do that kind of thing. I hope this helps you thinks more broadly about how you can boost your income and get some companionship at the same time. If you are enjoying listening to my podcast, please give me a 5* rating wherever you listen to podcasts. If I don’t yet deserve your 5*, please let me know how I can earn it. I hope this helps! Heather Have a money question for me?

If you have any personal finance questions send them to [ME] – I will answer whatever piques my fancy via a blog post.

Hi Heather,

My name’s Reena, I’d really like to know what my spending looks like relative to the average person, can you do a blog post or podcast episode on that? Thanks.

Great question Reena. At some point, everyone wonders: how do other people spend their money? Do I spend much more money on food or eating out or rent than other people?

Well, we keep pretty good records of this in the UK so this is what I found out from the office of national statistics website, hereafter, I’ll just call them the ONS: The numbers on spending can change a fair amount from one year to the next. The ONS releases a report of the UK’s household spending each year. For 2015/16 the average household spent c.£530/week, in 2016/17 it moved to about £537/week and in 2017/18 despite all the Brexit drama it shot up to £573/week. That it’s the highest it’s been since 2005. £573/week translates to £2,483/month per household. Basically, if your household spends more than £2,500/month before accounting for the portion of your mortgage that pays off the mortgage debt, then you spend more than the average household. This rate of spending translates to just under £29,800/year but median household income was about £29,000 in FYE 2018 so spending slightly outstripped earning – no mega news there. Average household size in the UK has remained at 2.4 people for over the decade – so it’s pretty stable. An interesting factor about spending is that it can frequently bear little relation to earnings so some people spending this amount will be relatively well off and could spend more but they choose to live beneath their means and some people spending at this level will be persistently spending more than they earn by taking on debts, e.g. by renting cars via leases or buying them via hire purchase agreements and so on. Threes notes for you:

Sidebar: the UK financial year starts on 1 April and ends on 31 March and the tax year starts on 6 April every year and ends on 5 April… In the FYE 2018:

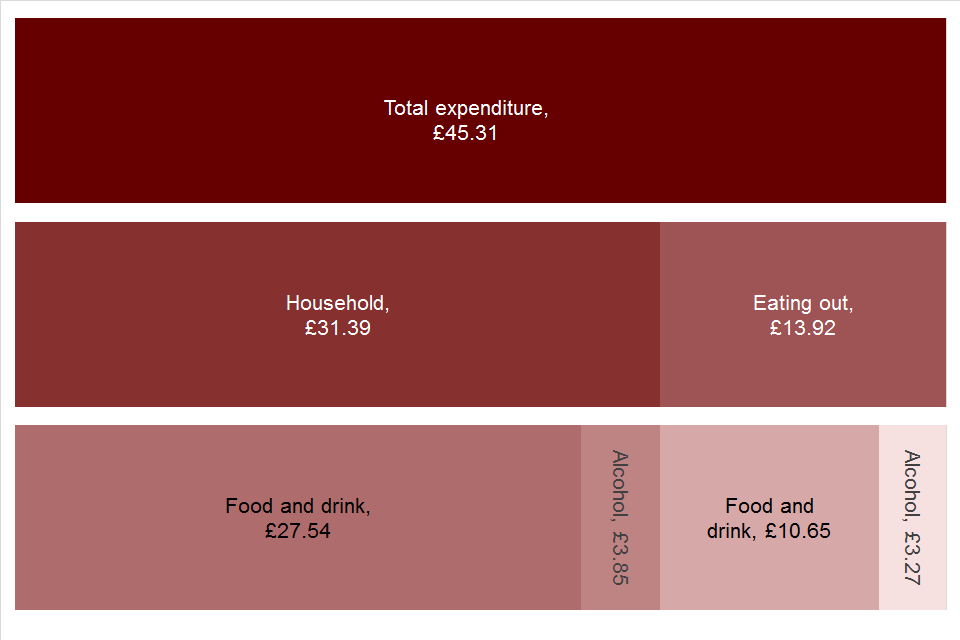

TRANSPORT In 2017/18 households spent £81 a week on average on transport – that’s about £350 per month. HOUSING The average UK household spent £217/month on housing and if you deduct housing benefit and related allowances this was only £156/month. Utility costs per month were: Electricity, gas and other fuels: £98 Water £40 Maintenance and household repairs £36 Total to housing is therefore: £330/month (156+ 98+ 40 +36) FOOD

What this says to me is that if you are a teetotal household of 2 grown children aged 18+ and 2 parents you can expect to spend £153/week {(27.54+10.65)*4} on food and drink at home and in restaurants, i.e. about £660/month. Alcohol consumption increase that to £785/month – so alcohol adds about £125/month to our 4 person household of 2 grown children and 2 parents.

Household food and drink expenditure per week

Really interesting, these stats suggests that our family should be spending £660/month but we frequently spend about half of this. The only month when we spent close to this is December when we spend £661 which is scarily bang on average. Outside of this mega month we’ve spent £190/month in our cheapest month and £330/month in the highest month outside of December and our food spend includes basic personal care stuff like roll-on and body wash which the ONS food spend number does not include.

Moving on… If you’re a teetotal average couple (i.e. no kids) you’re spending about £76/week on food at home and eating out, i.e. about £330/month increasing to close to £400/month if you buy alcohol. If you have two young children I’d count them as one and you should expect to spend £115/week on food and drink at home and in restaurants or about £500/month – this increases to about £590 per month if you spend money on alcohol. RECREATION AND CULTURE You know you are living in a privileged country when recreation and culture can fall into the top 4 spending categories. In fact, recreation and culture was the highest spending category for households in the North East and Scotland where it made up 16% and 14% of their spending, respectively. This was apparently driven by a few different factors, such as lower spending on transport and housing. Now, rather than give a narrative on each category, I will recommend you look at the table that I have compiled for you using the pretty awesome ONS website and see how the UK is spending. I’ll reel off the top numbers for you which I have split into weekly, monthly and annual spending so you can look at the metric that’s more relatable to you – some people work by the week, I prefer seeing things by month and year.

Weekly Monthly Yearly

Mortgage (for owners) 157 678 8,138 Rent (for renters) 108 467 5,606 Transport Personal transport 33 144 1,726 Purchase of vehicles 28 121 1,451 Public transport 20 85 1,024 Housing (net), fuel and power Rentals net of benefits 36 156 1,877 Maintenance and repair 8 36 426 Gas bill 10 42 510 Electricity bill 11 49 593 Other fuel 1 6 68 Water bill and misc. 9 40 484 Other expenditures Council tax, mortgage interest 47 202 2,423 Charity, cash gifts 14 59 712 Holiday spending 12 54 645 Licences, road tax, fine 4 16 192 Food and drink Food + alcohol-free drinks 61 263 3,151 Restaurants / catering 39 168 2,018 Hotels 11 47 567 Alcoholic drinks 9 38 452 Tobacco and narcotics 4 16 198 Recreation and culture Package holidays 27 117 1,399 TV+ video subscriptions 7 30 364 Newspapers, books, etc 5 23 276 Cinema, theatre, museums 3 13 161 Other recreation, e.g. photos 32 140 1,680 Households goods and services Furniture, carpets, floor 23 98 1,175 Routine household maintenance 7 29 348 Household appliances 4 19 224 Tools/equipment 3 13 151 Household textiles 2 10 114 Crockery and cutlery 2 8 99 Miscellaneous goods and services Insurances 18 76 915 Personal care 13 54 650 Bank fees, moving house, other 5 22 265 Personal effects 4 17 208 Childcare related 4 19 229 Clothing and footwear 24 105 1,264 Internet bill / spend 4 16 198 Telephone, fax, post office 14 61 733 Hospital / medical 7 30 359 Education Education fees 8 36 426 Secondary education 0 1 10 Nursery and primary education 0 1 10 TOTAL £572.6 £2,481 £29,775

I spent some dedicated time on the top things people spend money on to figure out how much is being spent according to a variety of sources; one of the sources I stumbled upon was the results of a survey carried out by powershop.co.uk on 2,000 people:

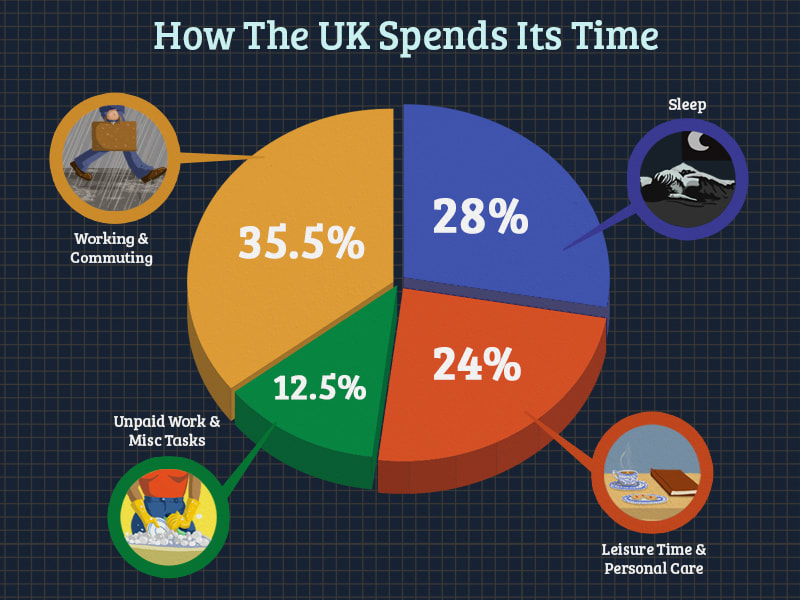

Interesting findings from the powershop survey include that 23% of households have a running direct debit for something they don’t use or need. This could be anything from a gym membership to a subscription to a streaming service such as Netflix. They also found that 20% of households delay switching energy suppliers even though it could save them up to £300 each year. How people spend their free time I also found it interesting to look up statistics to find out how the average person spends their time. This is very closely related to the question on how people spend their money. I found it extra interesting because I always wonder how everyone watches so much more TV than I do. For the UK:

So, 5.8 hours a day is spent on leisure and personal care. However, this masks a gender discrepancy as the average man has half an hour more free time than the average woman – 6.1 hours vs. 5.5 hours. The average American has about as one hour less leisure time than the average Briton at about 5 hours. Again American men spend more time engaged in leisure activities (5.8 hours) than did women (5.1 hours).

And the top 5 leisure activities are:

Key takeaways:

I hope this helps! Heather

Hi Heather,

My name’s Nicola. I’m fortunate enough to still have a job right now, most of my friends have lost their jobs and it’s made me realise that if I had lost my job I wouldn’t be able to survive at all. I have no savings, a few debts and spend all my earnings every month. What do I need to start doing, right now, to ensure that by the time the next crisis hits the economy, I would be able to survive regardless of my employment situation? Thanks for all the financial knowledge you share.

Dave Ramsey is having a field day with this COVID-19 pandemic and associated financial crisis! His very conservative school of advice is exactly the type of financial planning that you need to survive an economic crisis and it works especially well if you are in the type of job that is insecure and disappears in a market downturn. Go to his channel and he is all about the, “I told you so.”

Quite soon after the global COVID-19 pandemic hit in 2020, stock markets plunged to 2017 levels. Lots of investors got scared and decided to hold their money as cash, however, those of us that follow the Warren Buffet school of investing were not selling our shares, we continued buying as usual but at the now lower prices to reduce the average price at which we bought our shares. It turns out to have been a good idea because portfolios have bounced back very rapidly BUT it wouldn't have mattered either way, those of us with 15 plus horizon have plenty of time to recover and make fresh gains. Investing consistently over time and especially when stock prices are falling helps to reduce the average price at which you buy your shares, this is called “Dollar Cost Averaging”. Getting your financial house in order takes time; it is not an overnight thing. If you have a low income or significant debts it can take very many years indeed but these are the fundamentals you will not have regretted following in a world where the next crisis is always just around the corner. I don’t claim to have created a new financial world order; the principles I like and follow have been collected from many financial authors over the last fifteen years: 1. CREATE AN EMERGENCY FUND (and AD HOC FUND) Have an emergency fund of £1,000. This will cover most emergencies. If you’re a student, a £500 emergency fund should be sufficient. I used 60% of our £1,000 emergency fund to buy a freezer just before the UK went into COVID-19 lockdown. We only had a 70/30 fridge/freezer which means the freezer portion is tiny. I’ve personally always preferred fresh fruit, veg and milk to frozen or canned stuff so it was never a problem before but having such a low stock of food made me properly anxious and I am not even the anxious type. I won’t tell you the drama I went through to get what was probably Britain’s last freezer from a back alley warehouse shop but I do know I am not the only one that had some kind of emergency when COVID-19 hit. If you did use your emergency fund then please share how you used yours in the comments. If you didn’t have to use your emergency fund, that is awesome but I know you will have had a certain level of peace of mind by having had the £1,000 emergency fund set aside. An emergency fund is there to be used for any expenditure that you feel has to be made but had not been budgeted for: a car breakdown, an unexpected medical expense etc. How should you set up your emergency fund? Many UK savings accounts and current accounts are completely free so I would just add a savings account at your existing bank and build your emergency fund there. We also use the emergency fund for ‘ad hoc’ expenses so it gets topped up monthly to accommodate what we call ad hoc expenses. These are expected annual expenses that we prefer to pay for annually rather than by monthly direct debit. Ad hoc expenses include:

For example, if you figure out that these will total £1,800 per year, then you need to add an extra £150 every month to your Emergency Fund. Sometimes it will dip below £1,000 but because it’s topped up religiously every month it will get topped up again and if these annual expenses are bunched up around the same time of the year sometimes your emergency fund will be well above £1,000 but that is okay because you know that the money is there for a specific purpose. Paying for lumpy expenses annually rather than monthly gives you the same peace of mind as buying things for cash. You’ve paid for it, it’s done and frequently paying for it once a year is cheaper than setting up payments. Of course, if it costs exactly the same to pay monthly then that might be the better option to even out your cash flow. Alternative option: You could split bank accounts up further by having a separate "Emergency Fund" bank account and Ad Hoc Fund or Annual Expenses account; that way, the Emergency Fund remains sacred for a true emergency. 2. GET TO DEBT FREEDOM You will not ever regret having paid your debts off completely. Those that had zero debt when COVID-19 hit will have been best placed to weather the storm because they have no debt payments to be making in addition to their costs of living. If you want to tackle your debts systematically, get my “notes to debt freedom”. If you do have outstanding debt then create a plan such that in under 3 years, and ideally within 12 to 18 months you will be completely debt free. My notes to debt freedom will guide you through that process. 3. SET UP A CRISIS FUND The crisis fund is completely different to the emergency fund. A crisis fund is there to protect you against times of unemployment. The usual advice is to maintain 3 to 6 months of expenses to protect yourself against periods of unemployment. If you have a budget then you can easily calculate which expenses would continue whether you were unemployed or not. For guidance on creating your budget plus a downloadable spreadsheet to create a budget see my article, “Q&A: I hate budgeting – am I doomed to be broke?” Three months of living expenses is considered enough if you have a safe recession-proof job that’s likely to be easy to find again should you be unemployed for a period, think nurse, doctor, accountant, delivery person, bin man etc. If there is one thing that is being amply revealed by COVID-19, it’s the types of jobs that are safe and essential to our day-to-day life. A recession is not the only reason you might need to take time off work so that's why you need a crisis fund even if your job is recession proof. If you disliked your work environment because it was toxic, for instance, you might prefer to leave even if you haven't secured another job to move on to. If you send your children to private school, add at least a term of school fees to the crisis fund. If you have a property portfolio then add another three months of related expenses. You can make a reasonable judgment on this. If you have a large portfolio then this may not be necessary as you can make the judgment that some properties will always be occupied to support those properties that are not occupied. If you have lots of buy-to-let mortgages then do make a reasonable provision to accommodate continued payment of mortgages even if you lost a significant portion of rental income. If, when the COVID-19 pandemic hit you had:

If you have a mortgage-free portfolio of buy-to-let properties then you are feeling even more secure. With the stock market crash, it’s best to ride it out and not sell any of your shares. Selling would just convert paper losses to real losses. With a fully-outright-owned property portfolio you can enjoy some income stability in addition to having a healthy balance sheet as outlined above. To clarify, my household is not in the perfect situation either but we have been working towards it and will continue to do so. Our plan to get to the above situation is a 10-year plan and we are only at about year 2 right now. Thankfully we both still have our jobs so we can continue focusing on that plan. 4. GET/HAVE AN AFFORDABLE MORTGAGE The more affordable your mortgage is, the less financial pressure it adds to your life. If you are in a relationship, an ideal goal would be to have a life that is affordable on the lowest of your two salaries. So, whatever your mortgage is, that mortgage and all your other costs of living would be affordable on the lowest of your two salaries. Not entirely possible for all people. However, one way to work this is to have a very long-dated mortgage, e.g. a 30-year mortgage instead of a 15-year one, and in good times, make overpayments as though it were a shorter mortgage. However, in a crisis you would reduce payments on the mortgage to conserve cash. I reduced payments on one of my buy-to-let mortgages as soon as the covid-19 lockdown was put in place in the UK. The monthly re-payments for the last year were £2,500/month, which was £900 above the mortgage deal and in fact less than £500 of each payment was interest. This week I called the bank and reduced mortgage payments by £900 to conserve cash in case I lose a tenant, etc. This can work in exactly the same way for your personal mortgage. If I lose the tenant, I will call the bank and ask to pay interest only until the lockdown is over. My bank would probably be completely fine with that given my level of over-payments far exceed what they expected on the mortgage deal. In the past I have used this same type of cash flow management by getting an interest-only mortgage deal on our home and making excess payments with the intention of cutting back to interest only should times get tough such that we need to live on one salary. However, interest-only deals with a good interest rate are much harder to secure nowadays than they were in 2010 when I last got a residential interest-only mortgage. If your mortgage becomes unaffordable for any reason, call your bank and get a mortgage holiday. The media has made it sound as though mortgage holidays are something banks are doing as a one-off exceptional thing for COVID-19 but the truth is banks are always willing to give people payment holidays if they can prove that they are needed. Your bank would prefer not to have the hassle of repossessing a home. That wraps up the key 'big picture' things you can do to crisis proof your finances. >>>HABITS OF A LIFETIME THAT WILL HELP YOU SURVIVE THE CRISIS No matter what your personal finances look like, the one thing you can do right now is look at your monthly and annual budget with a fine tooth comb and figure out how to cut your cost of living – if you have a very expensive lifestyle, this is the time to think through your habits. If you want me to help you rework your finances, schedule a call using the “request a call button” on my coach page. Sometimes you just need an independent party to point out where you could possibly cut back, you know, the non-essentials you’ve began to see as essentials. Being confined to your home is not easy especially if you enjoy being out and about. The plethora of memes that have hit our whatsapp screens show just how much people are struggling to keep themselves entertained during the period of lockdown and social isolation. If your job, like mine, can continue as normal even from home then you have less time to get bored, however, this is the time when you can work on things that you wanted to do before because you don’t have a commute:

These are just a few ideas and I am sure you have more. Once the initial overwhelm and disruption to normal life created by COVID-19 subsides you will have the mental bandwidth to figure out how you can make the best use of this time. Oh and by the way, watching endless YouTube videos of all the skills you would love to develop, doesn’t count. Start working on something that you would never have otherwise had the opportunity to explore. In summary, to get your financial house in order:

Hope this helped. My prayers are with those that have lost a loved one or suffered a job loss at this already difficult time. Lots of love and adoration, Heather Have a money question for me?

If you have any personal finance questions send them to [ME] – I will answer whatever piques my fancy via a blog post.

Hi Heather,

My name’s Linda. I would like to have a comfortable retirement but I am not sure how much money I need to have saved up in order to achieve this goal. I am not particularly extravagant but I do want to be able to afford at least two holidays a year. I additionally don’t have access to a fixed workplace pension so I need to live within the means of my own investments and the state pension. How should I go about working this out? Thanks

Thanks for this question Linda.

There are a few ways to think about this. Firstly, when do you want to retire? The reason that this matters is that your state pension will only kick in at the state retirement age so if you retire earlier than this you will need to make up the difference from your own investments. You also need to consider your living situation during retirement. If you are likely to be married or in a relationship then you would have two state pensions coming into the household but not double the costs – for instance, utility bills don’t double with double the number of occupants in a home. You would also need to factor in that, even if you are in a relationship, one person will probably outlive the other and at that point one source of pension income may be lost. TWO WAYS TO GET AN INCOME IN RETIREMENT FROM A SAVED LUMP SUM There are two ways that your savings and investments can be used to secure your income in retirement: The first way is to buy what is called an annuity. The second way is to just draw down your income slowly over time. ANNUITY An annuity is a financial product that provides a guaranteed income for life. Essentially, you take a lump sum of money, give it to a financial provider and they tell you how much they can pay you for life depending on the features you want. For example they can give you a fixed amount every month for life, or they can increase that amount every year by inflation, if you want an annuity that grows with inflation the starting amount will be smaller than if you go for the fixed amount. You can also buy an annuity that covers one person’s life or two people’s lives, that is, once the first person dies the annuity continues to pay out until the second person named on the annuity also dies. Annuities used to be popular in the past but because interest rates have fallen drastically since the 2008 financial crisis they have not been so attractive. How much would you need if you were planning on retiring today, were getting a state pension and were planning on buying an annuity? According to this is money who in turn source a report by Royal London, you would need £260,000. “Royal London’s sums were based on the amount needed to bridge the gap between an £8,500 state pension and two-thirds of the £26,700 average salary.” Two-thirds of £26,700 is £17,800. This means Royal London are assuming that you would live on £17,800 every year: £8,500 of this would be coming from the state pension and £9,300 would be coming from the purchase of the annuity. These figures suggest the annuity is giving a return of just 3.6%. In my opinion, that’s a very poor return and not even worth getting the annuity. This is money also confirm in their article that if you plan to retire in 30 years’ time rather than today, this £260,000 becomes £400,000 and this further assumes that annuity rates improve by then. If interest rates are just as low in 30 years’ time as they are now and if we assume average inflation of 3% per year (which is what it has been historically), then instead of £260,000 you would need £630,000. Personally, I do not recommend the annuity route AT ALL. If you are happy to take a little risk then you would be FAR better off just drawing on the invested money. DRAWDOWN The most popularized rule for drawing down on your invested pot is the 4% rule. The 4% rule essentially says that if you drawdown 4% of an invested pot every year, you are unlikely to run out of money over a 30 year period. While the study that came up with the 4% rule used 30 years as the period during which a person would be retired, the general conclusion is that even at the end of that 30 years the money invested will have grown because the average drawdown rate of 4% is lower than the average growth rate of your investments. So, for example, if your investments grew by 7% in the last year then taking 4% means you are still ahead. The beauty of drawing down rather than buying an annuity is that whatever is left when you die can be passed on to children, charities or whatever you choose. With an annuity, the payments die with you. For example, if you bought the annuity of £9,300/year today and died next month, tata £260,000 – that’s it. The full benefit of your early demise goes to the financial institution that sold you the annuity in the first place. Rubbish, right, well that’s what you get for playing it too safe! If we take the £260,000 lump sum we have been using and continue with it for example purposes, then a 4% drawdown would produce £10,400/year in the first year which is better than the £9,300 you were getting from the annuity that ‘this is money’ talked about. Not only that, in the following year it could be that you will base the drawdown on a bigger number than £260,000 because the investments will have grown in value. The average growth rate of the stock market over the last few decades has been 10% before accounting for inflation. Of course, this says nothing about the future as stock market returns in the future could be better than or worse than this. Rather than working backward from what income a given lump sum will give you? Let’s figure out how much you will probably need to spend in retirement, that is, let’s work out your desired retirement income. Once we have your desired income we will subtract income from your state pension and any other pensions. We will then divide the gap by 4% and this will give you the value of investment assets that you need. SPENDING I’ll share two sources that I have found for trying to work out how much money you will need each year in retirement. SOURCE 1 – on how much money you need for retirement “According to research carried out by Loughborough University and the Pensions and Lifetime Savings Association (PLSA), workers who only manage to save enough for a retirement income that provides them with £10,200 a year (£15,700 for couples) will achieve a minimum living standard, those who managed to save enough for £20,200 a year (£29,100 for couples) will be able to live a moderate lifestyle during retirement and those who are able to save enough for £33,000 a year (£47,500 for couples) will be able to enjoy a comfortable retirement.” (source: moneyfacts.co.uk) This £33,000 a year (£47,500 for couples) includes holidays abroad, a generous clothing allowance and a car. These are the lifestyles that the Loughborough University and PLSA study creates:

I don’t know about you but I would like to target the comfortable lifestyle or better! Using the 4% rule, if you are targeting a comfortable lifestyle then:

Before you give up before you’ve even started because these numbers sound too hard to achieve, keep listening, I’ll give you an example at the end of how much you need to save now and it will sound much more achievable. If you are targeting a moderate or minimum living standard, you can calculate the equivalent numbers by following this formula:

As a reminder, the full state pension is currently £8,767.20 per year but I used £8,500 in my examples for simplicity. If you plan to retire based on the minimum standard of living at say 60, then when you start getting the state pension as well if you are a single person, you would be boosted to close the moderate living standard; and if you are in a couple, you would be boosted just beyond the moderate living standard by receiving two state pensions – assuming both people are entitled to the full state pension or close. SOURCE 2 – on how much money you need for retirement Using a report from the Joseph Rowntree Foundation, a respected charity, Fidelity.co.uk allows you to start of with a basic standard of living which costs £16,300 and allows you to add annual costs to this depending on the lifestyle you want. This £16,300 accommodates basic rental accommodation, basic costs for food, alcohol, clothing, water, gas, electricity, council tax, household insurances and other housing costs, public transport costs and an occasional visit to the cinema. The basic £16,300 cost of living assumes a single person not a couple. Within this figure you don’t run a car, you don’t eat out much at all, you don’t smoke and you don’t have internet access or paid-for film channels (I guess you would watch only free channels and have to go to the local library for the internet). Note that this £16,300 is higher than the £10,200 suggested by the Loughborough University study for a basic standard of living but lower than the £20,200 suggested for a moderate standard of living so we can call it basic Plus. I would guess the Loughborough study assumes you have paid your home off in their basic living assumption which could explain the difference. So, how do we boost the £16,300 basic income to improve our life style?

If you added on every single one of these extras, you’ll be at a very comfortable £37,500/year which is not too far off the £33,000 suggested by the Loughborough University study for a comfortable retirement. This would be equivalent to £54,000 for couple if we increase in direct proportion to the Loughborough study (37,500 * (47.5/33)). What level of investment assets do you need to achieve this? You need c.£940k if you are a single person or £1.35m if you are a couple before the benefit of a state pension. This £1.35m is very aligned with the £1.2m we got using the Loughborough University study. State pension income reduces your need to save and invest by about £200,000. If you keep a budget it might be easy to calculate what your monthly spending in retirement will be; just remove all the things you spend on now that you won’t need to spend on in retirement, like travel to work or rent or a mortgage payment if you plan to own your home outright at the point of retiring. There are a lot of numbers here but it’s more or less pretty straight forward once you have worked through it systematically. How much do you need to save now to live your ideal lifestyle and to hit your goal by retirement? You’ll need to take the next step and figure that out. If you want me to help you do this, request a call. As an example, if you are a 22-year old couple now and plan to retire at 67, you only need to be saving £285/month in total into pensions (that’s only £140/each). This has to be into pensions and not into an ISA as I am assuming you get the tax benefit of saving into a pension. My calculation assumes you get an average market return over those 45 years of 7%. If returns average 10% as they have in the last 45 years, you would completely overshoot and end up with a retirement pot of £3.7m – how’s that for compound interest?! If you are enjoying listening to my podcast, please give me a 5* rating wherever you listen to podcasts. If I don’t yet deserve your 5*, please let me know how I can earn it. I hope this helps! Heather Have a money question for me?

If you have any personal finance questions send them to [ME] – I will answer whatever piques my fancy via a blog post.

Hi Heather,

My name’s Grace. I recently started investing in stocks and shares and want to know the type of returns I should realistically expect? I’m especially interested in how long it will take for my money to double in value. Thanks

Great question Grace, thank you for asking it.

I will start by telling you a little story. When I first started working, I didn’t believe in long-term investing on the stock market. My philosophy was that you buy shares at a good price and when the price has gone up high enough, you sell, take the profits and move on. You know, the buy low, sell high philosophy. My philosophy has since changed. I believe you should buy shares and ideally never sell them except to manufacture a dividend while you are in retirement and I’ll give you two experiences that turned my thinking on this so radically. In about 2006, I bought about $2,000 worth of Apple shares. The price at the time was $70-something. I sold a couple of years later when the price had trebled feeling like a complete winner. If I had held onto those shares they would now be worth about $30,000 (maybe more, it hurts too much to sit down and calculate the exact amount) AND I would have additionally enjoyed about 14 years of dividends from Apple which I would have reinvested back into the stock as I always do. Note that the price you see now shouldn’t be compared to the price I paid directly because Apple had a 7 for 1 stock split in 2014. The way that works is that for every share you own, they split it into 7 shares and the price for each becomes one-seventh of what it was. The lower price is designed to make buying shares more palatable to smaller investors. Anyhow, had I held the shares to retirement, I could have either benefitted from the dividends to support my living or sold them slowly for income to support my lifestyle in retirement (this is called manufacturing your own dividend). FYI, I’m only 36 so retirement is still a while away for me as I enjoy working and don’t plan to stop working for a while yet. The second story is what happened to my pension savings from a job I had that had a defined contribution plan – this is a retirement plan that depends on how the stock market. Unlike the traditional workplace pensions the income in retirement is not based on a fixed formula. Anyhow, I didn’t know much about pensions at the time but a colleague called Karen Matthey told me that even if I didn’t believe in pensions I should pay in up until the match “because it was free money” – I think the company matched contributions into the pension scheme up to a maximum of 3%. I didn’t even know what “up until the match meant” – I was 24 and clueless but I listened to her and did just that. By the time I left that job in 2012 I had just shy of £30,000 in my pension account and within 5 years that had grown to £60,000, that is, it had doubled. I didn’t expect this performance at all and it’s at this point that I started taking the whole investing long-term thing seriously. Now, this made me curious to find how long it takes for an invested amount to double, which is exactly what you’re asking, Grace, and it’s at this point that I discovered what they call the rule of 72. With the rule of 72, you take the investment return you expect, divide it into 72 and that’s how long it will take for you money to double. So, if you expect a 10% return, then your money will double in about 7 years. (72/10); if you expect a 7% return then you money will double in 10 years, it ‘s a very easy calculation. Because my money doubled in 5 years, it’s also quick to calculate that I earned an average return of 14.4% (72/x = 5). And keep in mind that I wasn’t invested in anything fancy: all my money in this pension was in a passive global equity tracker, it still is – and my old employer pays all the fees so I just let that pension pot sit there, I can’t touch it until I am at least 55. If that money earns at least an average return of 10% (this is the actual historical stock market return), then over 21 years the money will double three times: 60k will double to 120k in 7 years (that’s by 2024, and it’s actually growing faster than this right now) which will double to 240k 7 years after that which will double to 480k 7 years after that (that’s by 2038 when I’ll be hitting 55). That’s insane, all from an initial 30k investment! After I figured this out I was annoyed at myself for not taking the stock market and pension investing more seriously and I’ve been making up aggressively for the last 3 years. At the end of the day though, it’s not about crazy returns for me, it’s about making a commitment to investing healthy amounts monthly. It’s very hard for most people, my younger self included, to believe that even £100/month invested over 30 or 40 years will amount to much but it is really surprising how these small amounts add up. What stock market return should you expect? There are no guarantees in the market, but the 10% average has been remarkably steady for a long time. That said, from year to year returns are very volatile. You will only get the average market return if you buy and hold, do not try to time the market. Personally, I model my investments in excel based on a 7% gross return (gross return meaning the return before adjusting for inflation) this would be about 4% after inflation of 3%. My general reading suggests that expecting a return after inflation of 6% is realistic: my 4% net return is therefore not over optimistic. If the experts are telling you to expect a real return of 6% that would make it a gross return of 9% because inflation tends to average 3%, using the rule of 72 you would expect your money to double every 8 years. Simples. To ensure you end up with enough money in retirement, perhaps base your returns on a lower number so that either you end up with more money than you need or so that you can retire early because you reach your goal much sooner. Key takeaways?

If you are enjoying listening to my podcast, please give me a 5* rating wherever you listen to podcasts. If I don’t yet deserve your 5*, please let me know how I can earn it. I hope this helps! Heather Have a money question for me?

If you have any personal finance questions send them to [ME] – I will answer whatever piques my fancy via a blog post.

Hi Heather,

My name’s Sam. Can you talk about financial independence and the steps one has to move through to get there? Thanks

Thanks for this question, Sam.

In the past, I used to think about financial independence in a one-dimensional way: you were financially independent if your income from passive investments exceeded what you need to maintain the lifestyle you want indefinitely. It wasn’t until I heard JD Roth the founder of Get Rich Slowly on Paula Pant’s Afford Anything podcast that I started thinking about financial independence as something that can be broken down into stages. I like his idea so rather than re-invent the wheel, I’ll share his wisdom with you and you can decide where you are on this continuum: Stage 0 – Dependence In the dependence stage, your lifestyle depends on other people for financial support. Absolutely everyone starts here, we are born fully dependent on our parents and people break out of parental dependence at different stage. I dare say you can break out of being dependent from parents and fall back into dependence in your 40s and 50s because of a life incident or poor planning. However, if even if you don’t live at home with family you would still be in the dependence stage if your spending exceeds your income. Following the dependence stage, stage 0, there are six stages to full financial independence in JD Roth’s model. The first three stages of the journey are the “surviving” stages. Stage 1 – Solvency You’re solvent if you can meet your financial commitments, that is, you have enough earnings to pay your bills. You will have reached this stage when you no longer rely on anyone else or on credit for financial support. You are a solvent person if your income exceeds expenses, and you are no longer accumulating debt. I reached this stage when I was 18 thanks to an academic scholarship. My scholarship paid for all fees and gave me a lump sum to cover accommodation, food and a plane ticket home every year. In December 2002 when my dad sent me a gift of money with my mother who was visiting me at school, I told her that from here on out I don’t need money from you and dad; I will survive within the means of my scholarship – I asked that they saved the money for my sisters’ education and I haven’t looked back since. My dad took that thanks and ran! While some people will reach this stage in their teens, as I did, most people reach this stage when they start the first job that allows them to leave home. Some never reach it and are dependent on others for survival from cradle to grave. Stage 2 – Stability You have achieved financial stability once you've repaid all your consumer debt and have some money set aside for emergencies, and continue to earn enough to save – you can think of your savings as your profits. You may still possess some “good debt” — student loans, a mortgage — but you've eliminated other obligations and built a buffer of savings to protect you from unfortunate events. Dave Ramsey suggests a buffer of £1,000 and I would agree with that as being adequate to cover most emergencies. I would recommend buying insurance cover for things that could cost more than this, e.g. buildings and contents insurance to cover damage to your home and your personal possessions. As I have never been in debt, again thanks to my scholarship, I could say I reached this stage at 18 as well. As a Malawian student living in Britain I had no credit history so no bank would give me access to a credit card or even an overdraft facility and no store would allow me store credit. You know how you get to stores and they ask you if you want to get 10% off by signing up to a store card? Well, I said yes and I got rejected with the net result that I always said no after that because I felt so ashamed when she walked back to the counter to tell me I didn’t qualify in front of other customers. Thank God for small mercies. I was an unsuspecting teenager in a foreign country and I don’t know what debt I could have landed myself in had that request for store credit gone through. Stage 3 – Agency The final “surviving” stage in JD Roth’s model is free agency. He describes this as the ability to work and live how and where you want. In the free agency stage, you've cleared all debt (including student loans and your home mortgage) and you have enough banked that you could quit your job at a moment's notice without hesitation. Apparently, some call this “screw-you money”. I was about to disagree with the free agency stage until I saw JD’s note that: “he knows first-hand there are times when you might prefer to carry a mortgage even if you don't have to. So, for the purposes of this stage, if you have enough saved and invested to pay off your mortgage, it's the same thing as not having one. Technically, I would say I initially reached this stage when I was about 30 because I had enough equity in a home I bought when I was 23 to pay off our home mortgage free and clear and I had enough passive income from a small business I set up at when I was 26 (but spent only 10 minutes a month on) to meet the other financial needs that I had at the time. I say technically because in practice, I would never have done that as even then, I knew I would probably want kids and I would need more money to give them the life I wanted them to have, essentially, even if you are in the agency stage but you know your future financial needs will be greater, you’re probably not fully there yet. In JD’s six-stage model to financial independence, you move from surviving to thriving in stages 4 to 6. As you work your way through these stages, money is no longer a safety net, but a tool to help you build the life you imagined for yourself and for your family. Each of the next series of stages assumes no debt or enough cash on hand to instantly repay all debts. Stage 4 – Security You have achieved financial security when your investment income can cover your basic needs. Investment income is money that you don’t need to actively work for; it arrives like clock work without any further input from you. So, in the security stage, based on how much you have saved and invested, you could live a meagre existence for the rest of your life. Even if you never worked another day in your life, you have enough to afford simple housing, basic food, essential clothing, and insurance. I would say we are currently working towards stage 4. If we both quit our jobs and took our children out of a fee-paying school, rental income would cover our cost of living and we have some decent savings to cover tenancy gaps BUT our whole life would come tumbling down if interest rates rose because of the buy-to-let mortgages and our mortgage so we are not here yet. In the security stage you should be able to cover all basics regardless what interests and other economic indicators are doing. Stage 5 – Independence Financial independence is the ultimate goal for most people. At this stage, your investment income is enough to fund your current standard of living for the rest of your life. You cannot only afford the basics, but you can afford some comforts such as holidays abroad too. You have “Enough” with a capital E. Stage 6 – Abundance In JD Roth’s sixth and final stage of financial freedom, you have “enough — and then some”. At the abundance stage your passive income from all sources not only funds your lifestyle indefinitely, but it grants you the freedom to do whatever you want. Besides sharing your wealth with others – which you should be doing whatever your stage of wealth but can really ramp up once you’re in the abundance stage – you can indulge in luxuries, explore the world. When you see me wearing a Patek Philippe, we have arrived here. Both children will be in university at this stage (think early 50s) and I will spend a full year of school fees on one watch! Okay, so in a world with starving children, even writing that doesn’t feel quite right – I’ll downgrade that aspiration to a Rolex which I could buy now but that will be my gift to myself for getting to Abundance! Jokes aside, the more money you can save either by clearing mortgages on your home or rental properties or by investing in stocks and shares and shares, the more your financial independence increases. As you become more financially independent your happiness levels are likely to increase because you can make decisions based on life fulfilment rather than what makes financial sense. Being financially independent doesn’t mean you will quit working, it just means that you can if you wanted to! Now, I can’t talk about financial independence without talking about the FIRE movement. FIRE stands for Financial Independence, Retire Early. The movement is a lifestyle movement whose goal is financial independence and retiring early. Most people agree on the financial independence bit of the equation but RE means different things to different people. To some, retire early actually means quitting work and living a hobby life of travel and blogging, to others it’s simply a reference to reaching the ‘Abundance’ stage of financial freedom. I am totally into the FIRE movement because I love how they’ve changed the meaning of what it means to live rich, many in the community live humble lifestyles in the secure knowledge that they are building real wealth. FIRE is not about conspicuous consumption it’s about real wealth and achieving meaning in your day to day life. Let’s wrap up with some key takeaways on what you can do to move towards financial independence?

The philosophy is simple and as you put ‘spend less’ principles into practice, it gets easier and easier not to spend over time. I hope this helps! Heather Have a money question for me?

If you have any personal finance questions send them to [ME] – I will answer whatever piques my fancy via a blog post.

Hi Heather,

My name’s Edna. I was wondering if you could talk about what net worth is? Why it matters and how I can improve my net worth? Thanks.

Thanks for this question Edna.

The net worth of a person is the value of what they own (these are their assets) minus the value of what they owe others (these are their liabilities). Now, most people don’t sit around calculating their net worth for the simple reason that most people don’t tend to think about their money situation but the calculation is very simple. I recommend you use a spread sheet when you do your calculation but you can also use a pen and paper. The only problem with pen and paper is that all the addition and subtraction is more tedious. Starting with the asset side, list down:

Personally, I don’t include things that fall in value like cars and computers but you can add them to the list as well especially if you own very expensive equipment that holds its value even when sold as second hand. I also don’t include personal possessions like books and clothing because I see them as being very transient and I would suggest you don’t bother with those type of thing either. Once you have listed everything that you own, find out what its value is and sum it up, this is your TOTAL ASSET VALUE. Then moving on to the liabilities side, list down: Your home mortgage Each of your buy-to-let mortgages All personal loans – from banks or stores All credit cards and store cards Money that you owe to friends and family Once you have listed everything that you owe, find out what the balance owed is and sum up all your liabilities, this is your TOTAL LIABILITY VALUE. To get your net worth subtract your total liability value from your total asset value, and voila! You have your net worth. For some people this value will be positive, for others it will be negative because the value of their debts exceeds the value of their assets. A negative value doesn’t mean you’ve been bad with money, it could just mean you’re young, have student debt and haven’t had a chance to build wealth, assets and earnings to pay off the student debt. A negative value also doesn’t mean you’re suffering. In fact, a zero net worth could be worse than a negative net worth. Lots of people in developing countries have no assets and no debts but they may be living a very difficult life without basics like enough food. In developed countries, access to cheap credit means people can live an amazing and lavish life although in reality this is sustained by debt. As long as the person earns enough to pay their interest every month this can go on for very long periods of time. And, the reality is, some people aren’t scared of debt, it doesn’t stress them out at all; what would stress then out is if they lost their job, or worse, reached retirement in this dire financial situation and found themselves pursued by people they owed money and possibly made homeless.

Why can knowing your net worth be valuable to you?

Because you can now track it, set a goal for it and improve it. If you have a negative net worth then you might want to aggressively tackle paying debts off. As you get rid of debts you’d also be getting rid of interest payments and would therefore have more disposable income to save and invest. Personally, I didn’t start intentionally tracking my net worth until I was 35 but I have always avoided debt, saved and invested from the very first year I worked so it wasn’t a trigger for me to be sensible but it definitely drove me to do better. Something weird really happens when you know your net worth, you become motivated to improve it and it makes it slightly easier to avoid excessive spending. How often should you track your net worth? I’d say once or twice a year is enough. Personally I refresh my asset and liability values on 30 September and 31 March – 31 March is ideal because it’s the end of the tax year and as I wanted equally spaced values, the second date became 30 September by default. When I track my net worth, I don’t regularly change the value of properties because it can distort the net worth calculation by inflating supposed increases in property value. If you plan on selling a property then you might be interested in updating the value but other than that, I’d just leave it. I also don’t update the value of defined benefit plans (aka final salary scheme or workplace pensions) because their value paper value can bear no relation to your ability to spend them. What is better is to get a general idea of what your fixed pension payment is likely to be based on the number of years you plan to stay in the job and keep this in mind as cash flow that you can expect at retirement. Also, ignore the state pension. You have no idea what the format of state pension will be when you get to retirement age unless you’re retiring in the next 10 or so years. I’d also just keep the number in mind. What does improving your net worth involve? To improve your net worth you either need to increase the value of assets or reduce the value of liabilities. Every time you reduce or clear a debt, you improve your net worth. Even if you aren’t saving but are focused on clearing personal loans and credit cards, you are improving your net worth. If you aren’t saving, or paying off debts but you own your own home and have a repayment mortgage on it, the act of paying your mortgage off means you are increasing your net worth. What’s your goal? Is it just to increase your net worth ? Or do you have a more specific goal, like increasing the value of assets in a specific area but not another, e.g. at a given point you might want more property and less shares or the other way round. Or is you ‘net worth’ goal more like mine? While some people will focus on increasing the gap between their assets and liabilities and don’t mind getting to retirement with debts. My personal goals is have the liability side of my balance sheet equal to zero by my effective retirement date of 50. At that point, I don’t plan to carry any liabilities. I will probably still want to work after that date but we will own our home and any rental properties outright and we’ll maintain our current no debt lifestyle. If you’re wondering how wealthy you are relative to other people in Britain I have some interesting data for you that I found on a BBC article dated July 2019: Apparently, wealth of £105,000 per adult would put your family in the top half of the population. By contrast, debt and a lack of property and pension wealth means the bottom 10% of families have less than £3 per adult. This says two things about wealth to me:

For the UK:

These statistics ignore age but we all know that wealth accumulation is a slow boring process so wealth levels tend to increase as people get older. So, it’s no surprise that 60-somethings (those born in the 50s) are the wealthiest age group, with average wealth equivalent to £332,000 per adult. Many 60-somethings are approaching the end of a career and have had time to accumulate savings, pensions and property.

Inheritance is going to be a big source of wealth going forward but again, property ownership matters a lot here. According to the BBC article which was itself quoting the Resolution Foundation, “millennials - the generation currently aged 19-38 - are set for an inheritance boom in the future. But it's a long way off, with the average millennial not expected to receive it until they reach 61.” It adds that, “Nearly half of millennials who don't yet own homes have parents with no property wealth, meaning they are unlikely to receive a significant inheritance. By contrast, those with home-owning parents are three times as likely to own a home by the age of 30.” Guys, if you hearing anything from this it’s beg, borrow, steal, scrimp and save and get yourselves on the property ladder to build a security blanket for yourselves – no pressure! Also, don’t shoot the messenger. Said BBC article had a large number of cynical comments under it – and a few helpful ones. How about wealth by race?!! … It was hard to find UK wealth data sorted by race but I did find home ownership stats: Overall, 63% of households in England were homeowners in 2016/18 (around 14.6 million households) Top three home owning groups in 2016 to 2018 were:

The bottom home owning groups were:

My group ‘Mixed white/black African were not much better at 34% All interesting things. So, in summary, if you want to increase your net worth without putting excessive effort into it, I would suggest as follows:

I hope this helps! Heather x Have a money question for me?

If you have any personal finance questions send them to [ME] – I will answer whatever piques my fancy via a blog post.

Hi Heather,

Happy new year! I’m a big fan of yours and have been following you for a while. I bought all your three books. I would like to open a stocks and shares ISA for myself and two children aged 16 & 14 but I don’t know where to start due to fear of risk. I want to invest 15% of my income in stocks and also considering real estate. I have seen some recommendations like Vanguard or Hargreaves Lansdowne but I’m clueless on what to go for. I am a nurse and the only debt I have is a repayment mortgage. I just finished paying off credit card debt. I saw your post on Malawi Queens. Please help. Thank you My name’s Angela by the way.

Angela – congratulations on getting rid of all your credit card debt, you must be super proud of yourself.