When you’re at one point in your life it’s often nearly impossible to imagine having much more than what you’ve got – or maybe that’s just my lack of imagination – anyhow, in this podcast I recount the steps we went through to move from our £385,000 beautiful terraced home to a £1.1m detached bungalow in the same neighbourhood.

We did all this in 2020 but, even as recently as in 2017, when I walked past the homes on the street where we now live, I thought actually living in one of them was pure fantasy for us and at that point, it was. It took getting a proper second income, a stamp-duty holiday and an all-time low 5-year fixed interest rate of 1% to achieve this, oh, and a few consumer loans for a short period. Was it worth it, 100%. One thing I forget to mention in the episode is that one of the key drivers was I saw already expensive properties getting more expensive and mid-priced (like our terrace) to low-priced properties appreciating very little in value or even falling in price – how does that work? I am not sure but I figured there was some kind of bifurcation in the property market with average incomes driving prices on the lower end and something bigger at play with bigger, more expensive properties – they tended to be owned by business people not restricted by average incomes, some people with inheritances and hence large sums to play with and people with much larger incomes…whatever it was, I wanted in. The funny thing is, if we sold our new house right now, we would be in a position to buy our old house mortgage-free AND still have £200,000 to £300,000 in change ALTHOUGH our old house has gone up by about £30-40k! Listen to the episode and let me know if you have questions. Here’s my property course on Udemy.

0 Comments

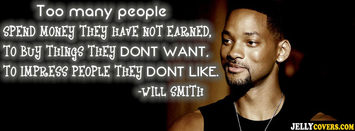

One of my best friends is loaded but you’d never guess she was unless you went to her house; she drives a clapped out car and she dresses well but very simply. Let’s call her Evelyn (not her real name). Evelyn once quit the 9-to-5 to pursue one of her hobbies but it didn’t work out the way she envisioned. She wasn’t making much money from the hobby and she ultimately lost interest in it so she decided to go back to the world of work. We met up for lunch and being the nosey person I am, I asked how much she was being paid, “£300,000 before bonus,” she said. For all those that need the conversion that is about $500,000 – and that was in 2012, she’ll be banking way more than that right now. Of course I was a little green with envy and for a brief instant I regretted leaving the world of banking, who couldn’t do with a couple of hundred thousand – I was happy for her too, though – if there’s one person who likes to see her friends succeed it’s me.  Apparently we’re all the average of the closest five people in our life – financially, healthwise etc. – success and failure both have a way of rubbing onto our friends. Anyhow, I digress. Two years into that new job she was still driving her clapped out car but she and her partner had bought a beautiful new home.They were paying down the mortgage and putting money aside so that they could retire early and pursue hobbies in their 40s. She’s about the same age as me so she was in her late 20s when she embarked on her high-paying career. My friend is extra special in how little she cares what people think of her. Almost everyone I know, myself included, would have spent some of that money on a lot more luxuries but not Evelyn. This got me thinking: why do so many of us care what everyone else thinks? Will Smith put it best when he said,“Too many people spend money they haven't earned, to buy things they don't want, to impress people they don't like.”  How much more financial progress would we make if we simply stopped caring what other people think and exclusively focused on ourselves. To a certain extent you will dress well and beautify yourself to look good for yourself but there is a residual amount of expenditure that’s exclusively done to impress others. This is why when you’re at home you’re happy for your hair to be stuck under a bonnet the whole day and hang around in your jogging pants all morning but you never step out looking like that. I’m not saying you should go out looking a hot mess but a little inner reflection regarding what you do for yourself versus the things you do simply to impress others despite your better judgment wouldn’t hurt. I don’t know about you but I think if everyone was a little more like Evelyn they would not only be happier but their bank manager would love them too. To caring less about what other people think!  Want to Build a 6-Figure Beauty Business from the comfort of your sofa? Then my course is designed for YOU!

"Beauty" includes a WIDE range of products from the not so obvious non-perishable foods and crafts to the more obvious hair, makeup, fashion, health & fitness.  A couple of months ago I wrote about how getting mortgages that are too large can keep people in the vicious cycle of the rat race. Yes, it is true that a mortgage can be a burden but there is also a degree of safety in owning your own home. If you plan wisely your mortgage will eventually be fully repaid and your cost of living reduced to very little. I believe that whatever your life plans are, you should invest in at least one property as a safety net. Even if you plan to travel throughout your old age investing in a home ensures that if for any reason you either change your mind or health requires you to stay put you have somewhere safe to live. Let me give you two life examples of people that I know. Their names are disguised for privacy: Maud Maud is 60 years old. She rents a 2-bedroom house in London at a relatively cheap rate of £600/month because she is locked into a very good contract that was agreed about 30 years ago. If Maud decided to move any similar property elsewhere in London, even within her own neighbourhood, that property would cost her £1,200 to £1,400 per month. Moving home is therefore not an option for Maud; she couldn’t afford the rent at the higher rate. The house she lives in has a resale value of £400,000 but it’s not hers to sell so that value is neither here nor there for her. If Maud had bought the house 30 years ago, she would have paid just £100,000 for it and would now have owned it outright for 5 years saving £36,000 in rent (£600/month x 5 years). She could now have either given those savings to her son who is 35 to help him get on the property ladder or done up the house which is now getting very tired.  She is tired of the décor in her house. Her landlord did it up 20 years ago and because everything still works well there is no reason for the landlord to update it. Landlords aren’t in the business of decorating simply to please their tenants’ tastes, they fix work that needs to be done to make a place liveable. Maud doesn’t want to decorate herself because she doesn’t own the house and could potentially be evicted for any reason, e.g. if the landlord decided to sell up. Anyhow, Maud made her decision not to buy 30 years ago and now she has to live with it. If she lives until 80 (which is more than likely nowadays) and if her rent stays at £600 (which would be VERY lucky) she has another £144,000 of rental payments in her future. Flowela Flowela is 26 years old. About 3 years ago, her and her soon-to-be husband decided to buy a property. They were lucky. They secured a 4-bed house for £240,000 in a small town and used money they had saved by living at home during their university years as a deposit. They have now been married two years and have slowly been decorating the house. It’s amazing what a lick of paint, some wallpaper and a new bathroom can do to a place. They love their home and are now settled into their jobs. Their mortgage payments are now £800 as they just re-mortgaged into a lower rate saving them £200 per month. Unlike with rent, mortgage payments can and do tend to fall. If they simply keep living as they do now, in another 22 years, just before Flowela and her husband turn 50 they will own their house outright. At that point their costs will just be bills and fun. They planned well and because they currently don’t have kids they are setting money aside to invest in another property that they can use to fund their retirement. They figure that if by the age of 30 they invest in a smaller place worth say, £120,000 or so and get tenants in there, those tenants can pay the mortgage down for them leading to a tidy little lump sum when they retire (if they decided to sell that place) or a monthly cash inflow of £600 to £1,000 which will fully fund retirement. Conclusion These are two real life situations. Which life would you rather live? Getting onto the property ladder may seem scary at first and like a big commitment but in the long run it offers an immense amount of security and peace of mind.  Want to Build a 6-Figure Beauty Business from the comfort of your sofa? Then my course is designed for YOU!

"Beauty" includes a WIDE range of products from the not so obvious non-perishable foods and crafts to the more obvious hair, makeup, fashion, health & fitness. When it comes to buying a property to live in there are too camps:

Most people in Britain fall under Camp Yes and you will find a lot more people (not a majority) in America under Camp No – the reason is the structure of Government taxes. In the US, when you buy a property in many States you continue paying quite a chunky annual tax. In Britain, you pay Government taxes when you buy the property and no property ownership taxes after that. This means that if you pay your mortgage off before retirement you can enjoy a much lower cost of living compared to someone who is renting and in the process avoid old age poverty. In fact, even while you hold a mortgage, with rents rising like crazy, mortgage payments are now frequently cheaper than rent. However, I have learnt that many people lumber themselves with a mortgage so huge that it becomes a lifelong burden. Most people buy the most expensive property they can afford to buy and frequently need two salaries coming in to keep up with mortgage payments. This is a form of wage slavery. According to Wikipedia, wage slavery refers to a situation where a worker's livelihood depends on wages, especially when the dependence is total and immediate. It is a pejorative term used to draw an analogy between slavery and wage labor by focusing on similarities between owning and renting a person. The fact is when you’re in a situation like this you will take ill treatment and all sorts from your job because you desperately need it and losing the job would cause you a lot of stress and trouble. When you’re in such a situation there are many adverse consequences:

Why do people get such huge mortgages? Usually it’s because they have their mind set on living in a certain, expensive location and they are unwilling to compromise; or perhaps they want a bigger house than suits their budget. A good amount of the time it’s because they want to look good to their peers and can’t take the “shame” of living somewhere that’s not “posh”. What should you do? I’ve said it before and I’ll say it again.

Decide how much you are ideally willing to spend on keeping a roof over your head and look at buying a home in areas where that will work. As I mention in my blueprint, 3 Steps To Quit Your Job, buying a home was part of my strategy in leaving the 9-to-5 and starting my own business.  One thing I don’t mention in the blueprint is that part of the strategy involved buying a home with a mortgage low enough to be easily affordable on one salary. In 2010 when we bought our home, we knew I was going to quit in two years’ time. This meant there could be months when cash was tight so we had to account for that. I have a property buying strategy that has worked superbly on two occasions: basically, you don’t buy in the really great area where you want to live, but as close to it as possible. As properties rise in value your area gets a massive benefit. Why? Because everyone that can’t afford the really nice area moves to your area instead leading to higher property prices. This strategy works in London where demand for property outstrips supply but may not apply if the converse is the case. I will admit that we had to stretch our budget by 30% because The Good Husband wasn’t happy with everything we were seeing at “my” ideal budget but in the end we found a great property that we were both thrilled with. Mortgages & Relationships If your partner is the one who wants to live in a pricey area and you know this will leave you chained to a desk job, show them this blog post. Hopefully you can re-work your strategy in a way that suits you both. How about Camp No? Sometimes you just have to rent because you have to live in certain places to progress in your chosen career. Many Camp No people can’t even dream of buying where they have to live because they simply wouldn’t be able to get the deposit together. If this is you consider buying a property in a cheaper location and renting it out so that you have the security of ownership then rent a pad where you need to live for your career (or whatever reason). I saw a good example of this on the TV show Real Housewives of Atlanta; a few people on the show rent because they need to live in the “it” place but they can’t afford to buy there. I think I have even seen a couple of shows where one or more of the contestants is being threatened with eviction for non-payment of rent. Eeek. Side note: Phaedra is my favourite – I think she is both the prettiest and the smartest. Nene is my second favourite and I think the rest of them are pretty forgettable, I don’t even know their names. I don’t watch dedicatedly but I do enjoy it when I find it on TV. Finally, for those that simply don’t believe in buying property at all, please leave a comment. I don’t personally know anyone and I would love to have a discussion with someone who has this viewpoint so I can see what their retirement strategy is. Whatever your point of view, share it.  Want to Build a 6-Figure Beauty Business from the comfort of your sofa? Then my course is designed for YOU!

"Beauty" includes a WIDE range of products from the not so obvious non-perishable foods and crafts to the more obvious hair, makeup, fashion, health & fitness. |

Heather on WealthI enjoy helping people think through their personal finances and blog about that here. Join my personal finance community at The Money Spot™. Categories

All

Archives

September 2023

|

RSS Feed

RSS Feed

Heather Katsonga-Woodward, a massive personal finance fanatic.

** All views expressed are my own and not those of any employer, past or present. ** Please get professional advice before re-arranging your personal finances.