by Girl Banker

Above all else, building a cache of contacts helps your career in direct and indirect ways. Five pointers on networking: 1. Attend networking events and aim to leave with about two business cards. Don’t stretch yourself thin by trying to meet with everyone; it’s much more useful to have a proper conversation with two people than ten superficial conversations. The two people you connect with are more likely to remember you later on. 2. Look engaged when you're talking to people Maintain eye contact, don’t keep on looking away and don’t check your phone – not even once. 3. Go to local recruitment events. If you manage to find out the names of any speakers in advance, do some research on them so that you can ask very specific questions, based on the speaker’s own experience of the industry.

4. If you don’t have business cards, get some made, even if you are still in university. I did this and found them handy in creating an impression. Let’s face it, it’s very unlikely that the investment bankers that you give your card to will actually call you. However, you will look like a real keeno if you have cards when most of your peers do not. Vistaprint produces good quality affordable cards. 5. Join any professional organizations or societies related to investment banking. You will probably find some in your local careers magazines or on careers websites.

You might also be interested in: networking part 2.

0 Comments

by Girl Banker Listen to the iTunes podcast instead. Seriously guys, a lot of people I know in banking spend without thinking. So despite the relatively high wage, by the end of their seventh year in banking, many don’t have any savings, property or anything else of relevance. What’s the point of working and blowing so much of your income that you can’t take any time out. There’s nothing fun or enjoyable about being cash-poor and asset-poor. Anyway, if you are serious about building a nest egg you need to have a strategy from day one. The moment some start their first proper investment banking job their attitude to money changes in a way that keeps them poor and job-dependent. These tips will ensure you’re not sucked into the same vortex. When I started in 2005 my analyst base pay was £35k or so. After tax, that was just over £1,900/month.  1. Decide how much you're going to save and stick to it I wanted to save £1,000 a month but in the end, I realised that this was far too ambitious. I still tried to do it for the whole of the first year; after 12 months I netted about £750 in savings per month including my sign-on bonus. That was still £9,000 in total, I was happy with that. 2. Decide what your first major investment will be and how much you will need for it This gives your saving strategy a purpose. I wanted to own my own property, badly! I was in luck, at this time interest rates were low and 100% and 105% mortgages were still plentiful. The dilemma: I knew banking doesn’t offer job security and I wondered whether or not buying a place at this early stage in my career might be too risky. I decided that it was risky but renting is even more risky. It’s far easier for a landlord to throw out a tenant than for a bank to make someone homeless. Decision: take the risk. At the time, I was reading Rich Dad, Poor Dad by Robert Kiyosaki and he went on and on about how the property you live in is not an investment because it costs so much to run. On that basis, I decided a two-bedroom property was the best solution. That way, I could monetise bedroom number two. Thanks, Bob! That was good advice. Boys, please note that a car is not an investment! (usually)  3. Open a share dealing account The moment I got my bonus, I worked out that I had more than enough for a deposit to buy the property I wanted. Dilemma: spend the excess or invest it. I decided to dabble in share dealing. I opened an account and threw £1,000 each at four stocks including Apple! I bought apple at $78/share and sold at c.$280/share a couple of years later. One of my worst moves ever! Key note: make sure you know all the fees that will be charged for share dealing. I prefer brokers that charge you for buying and selling stocks but don’t charge a quarterly or annual management fee of any sort. 4. Refuse to go out to over-the-top places There are lots of super expensive restaurants in London and their food does not necessarily match the price. When friends select a place to eat that will cost more than you are willing to spend, tell them so. There is no shame in that at all!  5. Refuse to subsidise other people’s alcohol needs I don’t usually drink any drinks because they contain too many empty calories. I drink water and tea mostly and a milky coffee (latte, mocha etc) once or twice a week as a treat. When the drinks bill comes I will exclude myself from it because I rightly have not been party to the consumption of any drinks. If I have drunk something, I ensure that what I am paying is more or less aligned with what I drunk. There’s no shame in that! 6. Steer your friends towards clubs that don’t have a minimum spend New York and London clubs love doing this: the best clubs will only allow you to enter if you agree to spend a certain amount. I refuse to pay. As a new analyst in training I noted that New York clubs really wanted more custom from girls. So a couple of guys with 5 girls were much more likely to gain entry than a couple of guys on their own. So, when the guys asked whether I wanted to go out, I just said I didn’t have any money. They would then (of course) say that they were going to fund the night out and I was game on! Sounds tight but I seriously didn’t have any cash at this time and didn’t own a credit card either so I wasn’t just being tight. Our very first wage was paid after the New York training programme.  7. If people call you tight or stingy, decide now that you don’t care Seriously, I don’t. I’m not even as cautious as I think I should be so any name calling doesn’t bother me one bit. 8. If you find yourself in a relationship with a profligate person, reconsider One of my guy friends found himself with a girlfriend who wanted Prada and Gucci gifts on the regular. He wasn’t even loaded: he’d entered banking at the height of the credit crunch and was comfortable but certainly not swimming in it. She was so money focused and I told him to give her the red card because their values were completely parallel – he eventually did.  9. Live like a student for as long as possible

This is the best thing you can do for yourself. After year one my base salary was bumped up by c.30% and I decided that as long as I didn’t have kids, anything above £1,900 per month (the analyst wage) would be saved. I lived comfortably on much less so this, to me, was reasonable. I now also had a mortgage so being responsible was even more necessary. 10. Don’t be scared to detach yourself from the pack Almost everyone that I went into banking with decided to live in Notting Hill, Chelsea, Kensington and other such affluent areas. Rents ranged from £1,000 to £1,500 for a shared flat. I decided this was way too much and plus, I wanted my own space – I was tired of sharing after university. I found a one-bed newly built flat in South London (Nunhead) for just £725 – with the water bill included. That meant I was paying less than half of what some of my mates were paying in rent. On most week days, I only saw that flat after 10:00 p.m. On weekends, I saw it a little more but not much more because I was either catching up on sleep or visiting friends. It was a pretty place and I’m glad I wasn’t swayed by where everyone else had decided to live. I hope this gets you thinking about your own philosophy on money management and the extent to which your friends’ decisions influence your own behaviour. Peace and chicken grease, Heather  by Girl Banker Listen to the iTunes podcast instead. These are the eight things that will get you a job in investment banking. I believe having seven out of these eight helped me get into Goldman Sachs as a newbie analyst. 1. Gain knowledge Read the news! At first you might feel like it’s a waste of time especially if you’re not interviewing yet but as time passes you’ll realize that some knowledge just sticks. Without a shadow of doubt, if you spend 20-30 minutes per day on financial press, your overall knowledge and feel for the industry will start to become well-rounded. 2. Come top of the Class or Course If you came top in any class or course - highlight it, it means you’re smart; smart = hard working (normally). In my second year in university, I came 5th in the Econometrics paper – you best believe that I brought that up interviews. Econometrics is hard and to come 5th out of about 150 people in a University of Cambridge class is the sort stuff interviewers are going to remember afterwards. 3. Be an Achiever - prizes, awards and scholarships Even if you’re not top of a class, any major prizes, awards and scholarships must be revealed when the opportunity arises. This sort of stuff shows that you are an achiever, bankers love to work with and be associated with high performers. 4. Be a Team Captain If you are captain of any sporting teams - don't forget to bring it up; out of any other credentials you might have, this shows you are popular and hence personable the most. Especially at the secondary school level, to be awarded the role of captain you need to be liked by the teacher and the people you will be in charge of.  5. High/school or College Start-up

If you have ever started a business, especially if it did well - mention it; starting a business or anything else shows that you have initiative and superior time-management skills. 6. Be the Linguist If you can speak several useful languages mention it; it’s impressive and it means you can be presented to a wide variety of clients. One time a VP of mine went to talk to someone and when he came back it wasn't the project we were working on at the forefront of his mind, he said, “Tiana is amazing, I was at her desk for 30 minutes and in that time four different people came to her desk with problems and she spoke to all of them in different languages”. She was fluent in Spanish, French, Portuguese and English. 7. Network and Get Contacts Look for events related to investment banking. If there aren’t any or enough at your own university make friends with people at nearby universities that can invite you to their banking events. 8. Get some work experience I have left this until last because many people applying to banking for the first time frequently do not have any work experience; sometimes they feel as though their work experience isn’t relevant. Mention whatever experience you have anyway even if it's a newspaper-round, there are likely some transferable skills e.g. a newspaper-round requires you to get up earlier and be more organised than your friends. The most crucial work experience is an internship the year before you graduate. Why then? Because if you impress the bank they will offer you a job that starts the moment you graduate. This means you can go back to your last year of university with peace of mind. You’ll be secure in the knowledge that there’s a job waiting for you at the end and you can just focus on your studies. Hope this helps! Peace and chicken grease, Heather  by Girl Banker Listen to the iTunes podcast instead. This post is related to, The most effective 10-step strategy for cold calling an investment banker. However, this post is concerned only with the actual phone call not the research and data gathering. 1. Sound upbeat A monotonous voice will bore the person you are calling and they'll want to get you off the phone as soon as possible. 2. Work on your high-pitched voice If you have a high-pitched voice practice talking at a lower tone. High-pitched voices are generally perceived to be irritating. 3. Before you hit the dial button, practice You can either do this yourself using the voice recorder on your phone or with a friend/family/professional coach. Video isn't necessary because only your voice matters in this case. 4. State your name. 5. State where you got the person's details if possible If you can say how you came to know of the person, that is very useful for building rapport. I found your details on LinkedIn is not a good line, you'll sound like a stalker. However, if you found details on the company's website, say so.  6. Mention a mutual contact, it will help to keep them on the phone longer

Check your LinkedIn profile to see if you do have a mutual connection. If so, call the person you know and ask them for permission to mention your name in the phone call. 7. State what you need help with. If you have done decent research on the person you might have found out interesting things about them, think about how you can spin their experiences to make yourself sound like a knowledgeable person on their industry and their job function and why you would be a good addition to the team or bank. 8. Get a promise. Before you get off that phone try to get some kind of a promise e.g. permission to call again, a promise that they will forward your CV to someone and, highly unlikely - but an agreement to meet or be interviewed. If you're not getting anywhere say something like: you sound very busy, I am so sorry to have called you at an inconvenient time, can I call you back at a better time? If they say, yes, ask when. Get the person's email if you do not already have it! 9. Follow up. If you failed to get anywhere on the first call, see what a second call might unveil. A third call is also okay but if that doesn't prove successful, that's where you need to stop. People in banking know each other and if you're branded a stalker it's not going to bode well for your job hunt. Happy job hunting.  by Girl Banker Listen to the iTunes podcast instead. If you haven't reached the penultimate year of university, you don't really need the information below. Get a copy of To Become an Investment Banker and follow the path that has been outlined in there. If you have graduated, are near graduation or indeed, well into another career, you might need to search more aggressively to get your foot in the door. 1. Decide which investment banks to target If you don't know which banks you want to focus on, have a look at the top 50 banks. GirlBanker.com/Banks has a lot of links that take you directly to the recruitment pages of the top 50 investment banks. The biggest banks provide a lot of information so any basic queries you might have will be answered on their website. 2. LinkedIn Lots of people voluntarily put their resumes/CVs onto LinkedIn. Before LinkedIn was publicly listed in 2011, you could get all manner of information; but because they now need to make money for their shareholders, some information is withheld from basic account users. They only show enough to entice you to upgrade to fee-paying status. If you have some generic questions about jobs at the company search for: "Investment Bank" + "Human Resources" "Investment Bank" + "Human Capital Management" "Investment Bank" + "Recruitment" Terms like investment banking division (IBD), or capital markets will not get you very far. Any big bank will have a huge IBD or capital markets department so you need to be a lot more specific than this. You should have a pretty clear idea of what teams you are interested in. Examples of good searches for team members: "Investment Bank" + "FX Sales" "Investment Bank" + "Derivative Sales" "Investment Bank" + "Credit Trading" "Investment Bank" + "TMT" "Investment Bank" + "Leveraged Finance" "Investment Bank" + "Healthcare" Normally, this only yields a name but not an email address. That said, read through the person's details and you might find their email included in their job summary. This is especially true for people that are actively trying to fill a role at the firm.  What information can you get on LinkedIn?

What do you do if the name is partly hidden? If you are completely unconnected to the industry you might find LinkedIn a little useless. Here are two workarounds: a) Over time, as you attend networking events make sure you add people you meet to your LinkedIn profile. I only joined LinkedIn in 2011 for the sole reason of building up a network and data access. I actively added people I know to my network and that allows me to see more information. b) Take whatever information you find to Google.  3. Google

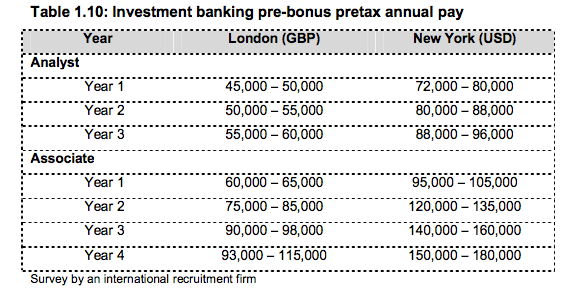

You can repeat the above searches on Google. In addition, a) Search for phone numbers: you're unlikely to get a direct number so just look for a reception number; b) Search for emails: it's easy if the person has a basic name. Most investment bank emails follow the format firstname.lastname@bank.com. Some investment banks have abbreviated emails i.e. @gs.com not @goldmansachs.com. Google what you think the email might be then email your contact. If the email you deduce is correct, it won't bounce back. c) Search the web for any information available on the person: to get a better picture of who the person is. It gives you more to talk about when you call/write. What do you do once you have a name, department and some basic details? 4. Call or write You can call via reception. Seriously, if you call the reception at most banks and ask to be connected to "So and So" they will put you straight through! I would say email is better than a physical letter in this case. Most people in an investment bank are extremely busy. Helping someone get a job doesn't yield anything for them (usually); any mail received will quickly be forgotten about and it will not be actioned. A letter followed by an email or a phone call might be more memorable. If you have a very creative idea in terms of how to wow them with a physical letter - do it!  by Girl Banker Listen to the iTunes podcast instead. This is the one question that everyone wants answered. Investment bankers' compensation is made up for two parts - base pay and a bonus.

Base pay is very transparent so let's start with that:  Excerpt from To Become an Investment Banker What about VPs and MDs?

Base pay for VPs and MDs doesn't rise hugely above the levels you see in the above table. Their compensation varies a lot more because of their bonus. Which banks pay the most? American banks tend to pay more than UK banks. UK banks tend to pay more than European banks. This is partly because big American banks make more but it's also cultural. The American dream is a capitalist one: make as much money as you can. Making money is synonymous with hard work in America. As you move towards the UK strong socialist ideals start coming into play. This is even more true for the rest of Europe. So what about the bonus? Bonuses are very variable especially during a recession. The bonus is more fixed at junior levels with larger differences between people at more senior levels. Bonuses can range from 0% to several hundred percent of base pay. Some websites will try to correlate pay with years in the industry but this is one industry where tenure matters very little. I have seen Associates earning much more than VPs because they are adding more to the bottom line. That's how it works. Whether you're an MD or a department head is of little consequence compared to how much your department or team earned for the bank. What does the structure of bonuses mean for you?

What does the structure of bonuses mean for your bank?

by Girl Banker Listen to the iTunes podcast instead. As an eager banker-wannabe whenever I heard the term "back-office" I imagined a category of overworked and underpaid workers toiling away in a windowless room at the back of a building! Personally, I find the term a little derogatory. In banking, the terms: back, middle and front office refer to how closely connected you are to the money train.  Front office Front office workers make the money. Their actions lead directly to more or less money being added to the bottom line of the bank. Front office workers will earn the highest bonuses because they essentially make the money and as such expect a higher cut. In theory, the more money you earn for the bank, the higher your expected bonus is. In a recession, bonus expectations will be lower overall but front office workers will still expect more than those further down the chain. Front office does not have to be client-facing e.g. traders usually do not see clients but if you are client-facing you will need to look smart and dress well for meetings. If you hate suits, this is not the best job for you! Front office includes:

Middle office Middle office workers are an integral part of making money. They directly support a deal but their actions have to be instigated by a front-office worker. A middle office worker cannot as a result of their own actions increase bank profits. Middle office includes:

Back office Back office includes any process-orientated roles. An efficient back office is vital because if clients don't get statements and confirmations on time they will hate your bank and could, on that basis, exclude your bank from deals. How can back office impact front office deals? Imagine you work on a company's small corporate finance team; you have ten bank relationships to manage. One bank consistently sends statements late. The statements frequently have errors and you have to call many times to get issues sorted - if it can be helped you're going to avoid doing business with that bank, aren't you? Back office includes:

So there you have it. When you're applying for jobs it can be a little challenging to decipher whether a role is front-office or not. This is especially true if you're applying off-cycle to a bank that has both a retail bank and an investment bank.

Use the above guidelines to help you decide how close you are to the money train. You want to get as close as possible.  by Girl Banker

Listen to the iTunes podcast instead. The very word "derivative" makes some people start running for the hills. It sounds scary, complicated, brain numbing. However, if you take the time to read a little about them, the majority of derivatives are easy to understand, particularly derivatives that are designed to hedge specific financial risks. Speculative derivatives can get a lot more complicated. A derivative is a financial product whose value depends on the change in the value of some other underlying product. Derivatives are primarily used for:

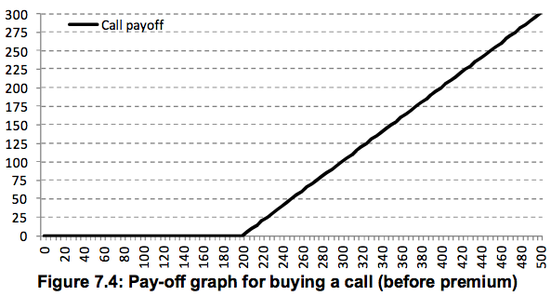

In the equity capital markets, the simplest derivative is an equity call option and in the debt capital markets the simplest derivative is an interest rate swap. So read: What is LIBOR? (it's an important variable in derivatives pricing) What is an interest rate swap (or IRS)? What is a call option or an equity call option?  by Girl Banker Listen to the iTunes podcast instead. An equity call option gives the buyer the right to buy a given number of shares in a given company at a given price on a given date (European-style option) or at any point with a given period of time (American-style option). Only the option buyer can exercise the option. To buy a call option is called going long a call and selling a call option is going short a call. Example Whilst Apple shares are trading at about $80 a share in late 2006 you decide to buy a call option that gives you the right to buy 1,000 shares in Apple Inc. at $200 anytime between 1 Jan 2010 and 31 Dec 2010. Buying out-of-the-money call options is much cheaper than actually paying the money to buy the shares outright. The call options are referred to as being out-of-the-money because the strike price, $200, is higher than the current share price of $80. If you buy this contract, you would be expressing the view that you believe in the company so much that you expect the share price to more than double over a four year period. This view would be the basis for buying the right to buy the shares at $200 in four years time, though the current value is only $80. If at any point in 2010 Apple shares exceeded the option strike price of $200, you could exercise your right to buy the shares at $200 and immediately sell them to lock in a profit. Let’s say each option cost you $1, this means you would pay a premium of $1,000 for this option contract. In Dec 2010, the Apple share price went over $320.

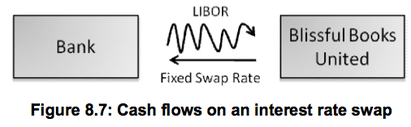

Excerpt from To Become an Investment Banker  by Girl Banker Listen to the iTunes podcast instead. The interest rate on money borrowed at a variable rate of interest, e.g. LIBOR, rises as the rate rises and falls as the rate falls. If interest rates are expected to rise, it is possible to hedge against the rise by entering into an interest rate swap (IRS) so that the floating rate is converted to a fixed rate. An interest rate swap (IRS) is an agreement between two parties to exchange interest flows. One party pays a variable rate (normally LIBOR, but it can be another rate, e.g. a government base rate) whilst the other party pays a fixed rate as set on the date that the IRS is executed (i.e. when it is entered into). The LIBOR payments are referred to as the ‘floating leg’; the fixed rate interest payments are referred to as the ‘fixed leg’. The diagram below shows an interest swap between a book seller, Blissful Books United (BBU) and a bank. BBU pays a fixed rate to the bank and receives LIBOR.  Excerpt from To Become an Investment Banker The maturity of interest rate swaps varies widely, they can be very short-dated e.g. 3 or 6 months or very long dated e.g. 30 or even 60 years. Very short-dated IRS and very long-dated ones are not very common. Maturities of 3-, 5- and 7 years are common amongst corporate entities.

The amount on which interest is calculated is called the ‘notional’ amount because this value isn’t paid upfront by either party involved in the swap. What would be the point of exchanging the same amount of the same currency? Payment dates occur periodically, typically every 3 or 6 months. On each payment the amount of interest due to be paid by each party is calculated and only the net amount is paid. For example, assume the fixed rate that Blissful Books United pays on the IRS is 1.50% and that Libor turns out to be 1.725% for a given period, who pays and how much do they pay? Assume a notional amount of $10m:

Normally, no upfront payment is required from either the bank or the non-bank counterparty to enter into an interest rate swap. Any costs and profits to the bank are incorporated into the periodic payments. To Become an Investment Banker goes into a little more detail on how the rates are arrived at, terminology and what an IRS term sheet looks like. If you want one-on-one coaching on interest rate swaps, please book a coaching package. In the week of June 25th 2012, the UK's financial services regulator the FSA claimed that some banks had mis-sold interest rate swaps to small businesses. Apparently, some small business claimed that they did not understand the risks that IRSs poised. |

Girl Banker®I created my investment banking blog in 2012 as soon as I resigned from i-banking & published my book, To Become An Investment Banker.

Initially published at girlbanker.com, all posts were later subsumed into my personal website under katsonga.com/GirlBanker. With 7 years of front office i-banking experience from Goldman Sachs and HSBC, in both classic IBD (corporate finance) and Derivatives (DCM / FICC), the aim of GirlBanker.com was to make it as straight-forward as possible to get into a top tier investment bank. I'm also a CFA survivor having passed all three levels on the first attempt within 18 months - the shortest time possible.

Categories

All

Archives

August 2017

|

RSS Feed

RSS Feed

Heather Katsonga-Woodward, a massive personal finance fanatic.

** All views expressed are my own and not those of any employer, past or present. ** Please get professional advice before re-arranging your personal finances.