One of my friends asked me for advice on where to put his money. As a matter of principle, I don’t give investment advice to friends because I know that I would almost certainly lose a friend if that investment went sour. Importantly, I am not a professional asset manager. That said, I do invest for my own account so I am willing to give tips that I find beneficial. To top up my knowledge, I picked up a copy of The Intelligent Investor by Benjamin Graham but I personally didn’t find it useful so I decided to set out a few of my own tips for successful investing. I have invested successfully in the past. My best success was Apple: I bought Apple at $78 in 2006 and sold it at about $280 in the 2009. At the time I felt like a don and I didn’t hesitate to show off to my friends. I sold my shares at the high of that time but if I had known they would be hitting $600 some day I would have sat tight and braced the hard times. Never mind. Personally, this is how I invest in shares:  1. Buy low, sell high. The saying is a bit clichéd but the whole point of investing is to make as big a profit as possible; to this end, you need to sell higher than where you bought. With this in mind, I usually decide on which region of the world I want to invest in, so if it’s the UK I am interested in, I download Bloomberg data for a given UK index e.g. the FTSE 100, for the top 100 UK companies. I then sort the list by the 52 week low, divide that by the current price and see which shares are trading near their 52-week low. Trading at the 52-week low does not immediately mean I will buy that stock but it gives me a good starting point. I hate buying shares that are near their 52-week high because I psychologically think they are more likely to come down. That said, I will still look at the names of shares near the 52-week high carefully to consider if it’s a pattern that might continue. 2. Consider your time. If you don’t have time to pick stocks carefully and to monitor your portfolio periodically, get an investment advisor. 3. Consider your skills. Do you feel comfortable investing? You don’t need to have a background in finance to understand the stock market but you do need to pick up a few books to understand how it works. If you don’t think you have the necessary skill-set, get an investment advisor.  4. Think long-term. I am not into speculating. I might give speculation a go at some point but if so I would allocate a small, fixed budget for that purpose. I personally think that you are more likely to make successful investments if you are looking for a stock that will perform well in the long-run than if you are shooting for short-term, fast profits. 5. Look at how much debt the company has relative to how much they earn. Companies with high levels of debt are more likely to run into problems. If there is a good reason for the high leverage then you need not worry too much but you still need to be wary. 6. Look for companies that produce something. Call me old fashioned but I prefer to invest in companies that have a tangible product. A product that people actually want and need and will keep wanting and needing in large numbers for a long time to come. If I think it’s a fad, I will not invest. #Facebook?! 7. Don’t sell just because the going gets tough. Share prices go up and they go down. If a company has done a major wrong and you think it could lead to bankruptcy, get out whilst you can. If you think that the market is just overreacting, then sit tight and wait for recovery. 8. Decide on your selling rules. Decide on what price you want to sell your shares at and if it reaches that price, try not to change the rules unless there has been a fundamental change in the company’s strategy that warrants a change in your selling price. People lose money because they get carried away with a good run and think it will last forever. 9. Consider the dividend yield. If you are interested in the size of dividends that are going to be paid make sure to go for stocks that pay higher dividends. However, if you are young, or are in a high tax bracket you should be more interested in seeing your asset base grow. Dividends can be a great source of income when you are retired but are less necessary when you’re in employment and earning enough to cover your needs. 10. Read the news. In this day and age, there is no excuse for not being current with global news. Knowledge will guide your investments.

0 Comments

If you’re solely depending on someone else, be it the Government or the company you work for to provide for your retirement, start thinking now about what percentage of the time you plan on choosing food over heating. If there’s one thing that can be learnt from the credit crunch, it’s that governments and companies are more likely to fail than one would like to believe. Let’s start from the beginning. Last week I was watching “Loose Women” on TV. The few times I’d flipped past the show whilst I perused what was on, I had perceived it to be an intellectually upmarket show where women discuss pertinent issues of the day. In fact, I watched it for ten minutes and had to change the channel because I couldn’t take the sheer ridiculousness of some of the things that were being said. One lady boasted proudly that she has never bought an investment property and owned only the property she lived in. She thought buying property was greedy evidenced by the property bubble and the credit crunch. It may have been the same lady, perhaps not, who stated that she’d grown up on a council estate but because her mother was quite an "aspirational" woman she opted to buy when Thatcher brought in the right-to-buy council housing. She went on to argue that her mother had disadvantaged herself in doing so because as a property owner she now can’t get as much out of the government. I think this was the point when I switched screens. Fact: most western governments are spending more than they collect in tax each year. It naturally follows that their deficit is widening with every passing year. The government cannot afford to pay the pensions that it thought it would be able to. Something’s got to give. To make up the difference two things will almost certainly happen:

I think if well planned, property is one of the best investments for retirement. However, you have to 1) start young and 2) have a portfolio. Paying off the property you live in is part of the plan but because you live in it, it can be hard to earn an income out of it at the same time. If you’re happy to rent rooms out in your own home then obviously that’s great. Most people prefer not to. WHY DO I THINK PROPERTY IS SO GREAT?  livingstingy.blogspot.com livingstingy.blogspot.com Leverage I paid a 5% deposit on the first property I ever bought. This means I borrowed 19 times what I put in. There is no other situation in which a Jane Average such as myself could get that kind of money. That was 6-years ago when I was 22. A good chunk has been paid down already just by making small monthly payments each month.  Youth The average mortgage is 25 years long. If you plan to completely retire at 60 or 65 it means that any property purchased before the age of 35/40 could feasibly be fully or at least mostly repaid.  Unearned savings Property income is taxable but the interest payments and any reasonable costs e.g. estate agent fees and insurance can be deducted before tax. If you’re being taxed at 40% you’ll still be receiving 60% of the profit. For example, if after interest and other costs you have a £500 profit, the government gets £200, you get £300 which you can use to retire the mortgage or use in any other way you see fit. Regular repayments of the mortgage using this unearned income mean that over a 25 to 30–year period you could have a solid asset base built almost entirely of other people's money.  Annuity If you manage to build up a property portfolio of say four houses by the age of 40, excluding the one you live in, it’s possible for those mortgages to be fully repaid or mostly repaid by age 60-65. If those four properties can be rented out at £500 each, that is an income of £2,000 per month. This is enough for an old couple to live on comfortably. Even with out a capital gain, a pension is insured. By this point, your home will be fully paid down too so the main expenses are food and utilities (gas, electricity, water, insurances, phone and internet) with plenty left over for a holiday or two. In addition, the property portfolio will be (almost) 100% equity so you could decide to sell up and put that money to better use. You’re financially flexible. The interest-only view I know some people who subscribe to the view that you should never repay a home, just get an interest only mortgage and own the house for capital gains. I have two views on this:

Job done. Now, is that greedy, I ask? I think with foresight and delayed gratification, anyone can achieve this. I don't think you need to be particularly brilliant at anything nor do you need to be earning big bucks. You just need to take advantage of a bargain when you see one and interest rates when they are low. Some of my friends laugh at my shopping at Primark but I tell them, less now for more later…this is my mantra, join me so in retirement we can all be sun bathing in the Bahamas sipping on piña coladas with not a financial problem casting a shadow over our retirement. If you haven't read Rich Dad, Poor Dad already. Please do get it, it help me to form some of my views on money. Don't just read it, absorb it and digest it. Links to Amazon.com and .co.uk below.  To Do What You Want Rather Than What Makes You Money Is A Luxury Preserved For The Privileged Few12/2/2012  If you know someone that says this it is more than likely that they grew up in a well-to-do home and never knew ‘want’. They see their ‘socialist’ views on life as something that sets them above other people, but seldom do these sanctimonious individuals pause to acknowledge how much of a privileged position they are in. Most people do not have the privilege to follow their hearts. To do so would be selfish and indeed self-indulgent. Money is not evil, it is an enabler, having a little money can be the difference between dying and having a few more breaths on this earth. I grew up in a poor country and was naturally frequently exposed to poverty and want. Yes, I fully acknowledge that I was raised in a relatively wealthy family but when you come from somewhere as poor as Malawi, that doesn’t mean you’re completely sheltered from the vagaries of misfortune. Fortunately for me, the things I enjoyed in life steered me towards a career that earns decent money. If for some reason I decided to follow a self-indulgent path that did not earn money, I would at the same time be taking myself off the path that would enable me to one day contribute in real, monetary terms to my family and to my country. Yes, you can contribute in non-monetary terms but I dare you to say that to the mother that hasn't been able to feed her children for two days. When you're poor, money to purchase food and shelter is all that matters. It consumes your every thought and effort. The needs of my own life are simple and I continually try to temper them. My biggest fantasy for when I have a real amount of money is to build a series of little libraries in Malawi because it is only through study of the written word that people can gain freedom from poverty. Most people in Malawi and indeed in many poor countries follow the path that makes money because they don’t have the choice. They need and want to help their family. The money they earn frequently goes to help with the school fees of siblings and to purchase medical supplies for any family members that are sick. Most poor countries cannot afford a state funded medical system. Free education if it is available is frequently atrocious, you wouldn’t wish it on an enemy let alone a loved family member. I know many including Steve Jobs proclaimed that you should follow your heart not money. I agree that this is an ideal position but most lives are less than ideal. Your family are the only people that love you unconditionally. The more selfless amongst us put our families first and ourselves last and in many cases if given the choices: 1) low-income fulfilling career but unable to contribute towards the extended family or 2) high-income less fulfilling career but able to contribute towards the extended family Most people would choose option two because they have to. So, for those that are fortunate enough to come from a background where they don’t have to make this choice, please stop being so self-righteous and count your lucky stars.   Source: Wikipedia Source: Wikipedia Sometimes my life reads like a Hollywood movie. Last week my home was almost robbed. Something I thought only happened to other people; indeed, some events, I expect (and prefer) to see only on film. Roused by a strange sound my husband walked into the kitchen to find a South London chav trying to break the window open with a crowbar. Minutes later my house was occupied by the police, sniffer dogs and forensics. We were lucky though, we learnt a cheap lesson, two other homes in the neighborhood were not so lucky. People may blame such behaviour on the recession, a lack of jobs, desperation, life but whatever the reason is we responsible citizens need to protect ourselves against such selfish acts. Thieves have little regard for the hard graft that underlies a purchase. I was a little blasé about the almost-robbery until our neighbor’s CCTV showed that the thieves specifically targeted us. A lady drove by and knocked on the door to check if anyone was home – my husband didn’t answer so she drove off and returned three minutes later to drop off a lad that never reappeared on the CCTV screen. When my hubby caught him, he leapt over the back fence. If this chav had found our car keys the police reckon he would have loaded anything that he could sell into our own car and driven off with it! What can you do to protect you and your family: 1. Lock interior doors when you leave the house. This makes it harder for thieves. Once they get into one room a locked door means they can’t get into another room. With the new obstacle the thief may get turned off and leave because the question in their mind will be “if they bothered to lock this door, what other obstacles will I have to get through?” 2. Get a personal alarm. If a thief ever manages to get close to you an alarm may scare them off because it attracts attention. 3. Get a safe and lock all your valuables in there: laptops, iPads, cameras, car keys. Make sure it can be bolted to the floor or a wall so that it can’t simply be carried off. They are not as expensive as one might think, £150 - 200 will get you a decent one. 4. Get a domestic alarm system with PIR movement detectors. Think: Mission Impossible. If the thief walks past a ‘sensored’ area or breaks a door or a window the alarm is triggered. Look for systems that can be enacted remotely with a fob. Again, about £200 is enough for a quality alarm system. 5. Lock your bedroom door when you go to bed. I used to love sleeping with my bedroom door AND window open! I gave up on having the window ajar because my husband hates that, he gets cold easily. After the almost-robbery we started locking the bedroom door too but that only lasted until we got the alarm system. If you don't have one, lock your bedroom door. My colleague knows a man who’s house was broken into, the intruder went all the way to his room, gave him a light tap on the shoulder and said, “We know you have two kids in the next room, give us your valuables and we’ll be on our way!” There’s only one reasonable response to that situation, you shouldn’t risk your children’s lives – give what you’ve got! 6. Get CCTV. Quite pricey but if you have expensive kit in your house that you need to protect, it could be worth it. A quality CCTV system will set you back £500 at least, a grand easy. 7. You can insure some goods against theft but some things are irreplaceable like family pictures that haven't been backed up elsewhere. I wish we could all live in a world where front doors are left open without concern. I grew up in such a world but things have changed radically since. Some people have zero scruples, they blame the world for their problems: what they can’t get for themselves, they will take any way. You’ve been warned.   Source: insurancequotetips.co.uk Source: insurancequotetips.co.uk Before I became a working adult I used to think that all insurance was a big scam: you pay loads of money every month to cover a most unlikely event so what’s the point? If I was ever asked to buy insurance I said ‘no’ without so much as thinking about it. I relayed this view to a colleague of mine and he told me that he always insures what he cannot self-insure and in his own life that was mainly his home. By this, he meant that if his house was destroyed by some accident he couldn’t afford to rebuild it in the same way he could easily replace say, a stolen phone with another phone. He didn’t realize it but those words held sway with my financial thinking from that moment onwards. Having been converted, buildings insurance became my first ever purchase of insurance. After a few home accidents: a broken toilet one time, plumbing damage the next, I decided that I also needed home care insurance; these type of incidents happen when you least expect them to and have a knack for hitting you when you’re the most broke. If you ever have plumbing trouble calling out a plumber to fix the issue will set you back £200-£300 easy, and that’s if it’s a simple problem. Just before Christmas I had to make two insurance claims, a property I let out had a bad leak so the home care insurer had to be called in; then, because of serious water damage to the ceiling the buildings insurer had to come and correct that permanently. My nifty filing system meant that I found both insurance contracts within ten minutes and knew exactly where I stood from a financial standpoint. If I hadn’t been insured I would be looking at an outlay of£4,000 to £6,000 and the likely loss of a tenant. I don’t have that kind of money just sitting around. As it stands, I only had to pay a £250 excess. Home care and buildings insurance cost a combined total of £500 per year. This figure sounds exorbitant but as the above example shows when something goes wrong it could cost much, much more than that to fix. I can live without my phone, laptop, TV, even my couch but I need somewhere to live so I am willing to insure my home whatever the cost. In late 2006/early 2007 I even took out private unemployment insurance that would cover my mortgage for 12 months if I ever lost my job. At £12-15 per month it was ultra cheap and the knowledge that my mortgage payments were covered gave me great peace of mind when the credit crunch hit in late 2007. Unfortunately, I had to cancel it in 2009 when the premium was trebled due to the recession and the large number of unemployed but by then I felt somewhat more secure in my new job. So, next time you’re contemplating whether or not to buy insurance, ask yourself if you can self-insure the item in question. If not, buy the insurance.   Source: thedigeratilife.com Source: thedigeratilife.com Attitudes towards money and suitable clothing Sometimes I think I live on a completely different planet to everyone else. We’re sat talking about shopping and my friend, Amelia, who lives in Dusseldorf complains about the lack of shopping variety there. She used to live in London and says she misses Karen Millen, Whistles and a couple of other (high-end) high street shops that she used to frequent. I have never even walked into any of the shops she’s just mentioned except Karen Millen where I bought a dress once in 2007; I still wear that dress. I see them as being too over-priced and plus, I have other priorities. £100 when shoes are on sale? No way. I could get three or four great quality shoes for that £100. Amelia reminds me of that age-old argument about having to use your feet every day and hence the necessity of treating them well. I tell her that her reasoning doesn’t hold water. Billions of people on this planet have been wearing plastic shoes and in many cases no shoes at all for donkeys years with no orthopaedic problems to speak of. Anyway, I digress. I know she comes to London a few times every year so I suggest she merges all her shopping into those trips. “You only need to do a proper shop once or twice a year, right?” “Umm, no, like once or twice every month.” I’m quite astonished . Personally, I shop according to need most of the time: a wedding, a major party or my work clothes looking tatty. Then once a year I will do a major shop spending about half a months’ salary in one go and then no more. I didn’t even do one of those this year, I opted instead to invest in a fabulous wedding dress. I rarely go clothes shopping outside of the event-driven and annual wardrobe upgrade. Weird, right? That’s what I am thinking right now. Lots of women seem to go shopping all the time and my question is, where is all that liquidity coming from? Bernard overhears us and gets interested. He comes over to seek advice on which Louis Vuitton handbag he should get his new wife for Christmas. Hello? Louis Vuitton? I remind him of the several thousand pounds of debt he still has on his credit card from his wedding earlier in the year and he says he’ll ask his pa for a bit of dosh. Ask your father for money when you are not even in desperate need? ! I won’t even get into that. Another friend, Josephine, joins the conversation at this point and I confess to all three that I feel guilty when I spend too much on myself. I believe that coming where I come from (i.e. Malawi) I can only remain true to my roots and to the meaning of life with simplicity and generosity where I can afford it. I said that rather than buying a £600 Louis Vuitton handbag, if I had that cash sitting around, I would much rather call my mum and ask her to find me someone who needs secondary school funding. You’re by now thinking, well, if they have the cash, why not? Thing is, I’m not sure that they do. Amelia asks why I have such a stark view on money management although I earn ‘loads’ more than her. It’s simple. I think what I value the most in life (besides friends and family) is freedom, the freedom from being tied down by a job or by bills or by a mortgage. Whatever excess money I have, I find some way to invest so that as soon as is possible, I will own my house outright and all bills will be paid for from unearned income - income from investments. Buying myself that freedom will mean more time to enjoy with family and to pursue hobbies and charitable causes. For me, this obsession with clothes and nice cushy things seems insane, absolutely crazy. Our conversation veers into Amelia’s dislike of non-natural materials. “I only wear cotton, wool, leather, viscose and other natural fibres. Nothing that starts with a P.” “So you’re high maintenance, basically.” I chimed. “No but if I can get the natural fibre, I will, they feel better.” “I haven’t noticed any major difference in how I feel in different clothes.” “Of course they feel different. If I find a really fabulous dress but it’s the wrong material, I won’t buy it.” For the first time, I come to the realization that the material of clothing is a major factor in some people’s shopping decisions. I judge clothes visually. If the quality looks good visually, I’ll buy it. I have never even thought to check the label to ensure it’s natural! Is that just me? Please tell me it’s not. Geez, a whole other world has just opened to me. I’ve just had to check what my sweater is made from. It says 100% cotton Phew!, I’m not being judged. But even if I was, I have never cared, no point starting now.   Image from frugaltownandcountry.com Image from frugaltownandcountry.com ...Or at least that’s how I felt for the first hour after watching The Ultimate Guide to Penny Pinching on TV. They rounded up a select group of Britain’s best penny pinchers and I was astounded at the extent that some people will go to, to save a penny – and in some cases it was literally a few pennies:

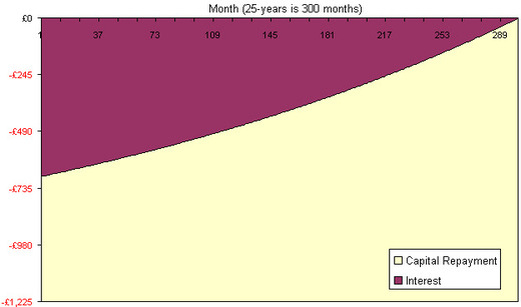

Time efficiency There are only 24 hours in a day. Part of the reason I work is to buy myself some leisure time. I have a plethora of hobbies which I want to pursue in my non-working hours – reading, writing, spending time with my family and friends, sleeping?! Rather than spend an hour going through price comparison websites to decide where to shop, I can do one of the above. Productivity I thought, if these people chased enterprising ventures with as much earnest as they do the bargain hunting surely they would by now be raking it in? One can spend so much time trying to save a buck when in fact, spending the same amount of time trying to find a new revenue stream would earn you two bucks. Finally, Peace of mind Sometimes people underrate the importance of having peace of mind. Ms Coupons admitted that whenever she heard there was a deal to be had somewhere she just had to go there and get it – even if she didn’t like the product in question! Come on? I wouldn’t want to have that kind of stress. She felt she was being wasteful if she didn’t take advantage of a deal. My opinion on the matter is – let’s pursue frugality but let’s not be obsessed about it. I’ll try to be generous of heart but I won’t be wasteful; I’ll try to save money but I won’t make it the bane of my life.  There was an interesting article on pensions in City A.M. a couple of days ago. Although I agreed with most things suggested by the article such as, the earlier you start saving towards a pension the better (even if it is just a small sum to start off with), I thought property was discussed in an overly simplistic manner. It was noted that 13% of those surveyed said their property was their pension. In pointing out that property does not necessarily provide a better return than the stock market, the article quoted James Sumpter of Bestinvest: “Contradicting common misconceptions, Sumpter notes the FTSE All Share index rose 1,038 per cent in the last 25 years since 1986, while over the same period house prices have risen by just 367 per cent – 427 per cent in greater London.” Point 1: Leverage really juices up the return on property The figures above give the impression that a £10,000 property investment would have grown to a value of £36,700 25-years later whilst the same investment in the FTSE All Share would have mushroomed to £103,800. However, if Joe Bloggs wants to buy a property he can borrow a good portion of the money needed to make that investment from a bank but Joe Bloggs would not be able to borrow as easily to invest in the stock market. This is best understood with the help of an example. Just prior to the 2007 credit crunch 100% loan-to-value mortgages were plentiful. That is, you could borrow all the money needed to buy a house and sometimes even more. My friend bought a flat in 2006 for about £250,000 and all she put in was about £5,000 to cover the tax, legal fees and other purchase costs. She lived in the house for 3-years and then let it out because she was going abroad. The rentals she’ll get from the property over a 25-year period will likely exceed the mortgage repayments required but for simplicity, I am going to conservatively assume that the rent received exactly equals the mortgage and maintenance costs including the mortgage payments she made herself during the 3-years she actually lived in the property. If history repeats itself and property returns 367% over the next 25-years, her profit will be £912,500 (that is, £250,000 x 367% - £5,000). Had she put the same £5,000 into the stock market, her profit would only have been £46,900 (that is, £5,000 x 1,038% - £5,000). That huge stock market return isn’t looking so juicy in comparison anymore, is it? Point 2: the return statistics ignore some of the flexible cash flow opportunities that property offers in a way that the equity market does not and cannot A little background: some of my thinking on property has partly been shaped by Robert Kiyosaki’s, Rich Dad, Poor Dad, I was reading that book at exactly the time that I wanted to buy my first property. Kiyosaki planted the seed in my head that the house you live in is not necessarily a great investment from a cash flow perspective. From the point of purchase, a home bleeds cash out of you due to the deposit required, legal fees and other transaction costs; then on an on-going basis the property also needs to be maintained. I was planning on buying a one-bed property at the time because that is all I could afford in the areas that I wanted to live but once I read Kiyosaki’s take on property, I changed strategy and shopped around for two beds. Although I was stretching myself thin I knew bedroom two could be let out to help with the mortgage. This is exactly what I did. I was also very lucky in managing to find fun, like-minded housemates every time the room was free. A pensioner can do exactly the same thing if they don’t want to sell their property. If there are free rooms in the house due to children fleeing the nest, why not let those rooms out to earn more money. With an equity portfolio, dividends only occur at very discrete points in time and indeed in a recession companies are prone to cancelling their dividends. I know of another person who built a fabulous house on the coast somewhere in Australia. Every summer she worked abroad for three months during which time she let the property out. Those three months produced enough rent to pay off the entire year’s mortgage. Of course this option is not available to all of us but it is another example of the versatility of property. Final point: buy to let Many cannot afford to buy more than the property that they live in, however, those that can may intend to hold the property indefinitely and let it out for income during retirement. There is a certain obsession in Britain with climbing the property ladder: people buy one property, then once it increases in value they sell it to buy a bigger, better and more expensive property that they previously could not afford. Some people continue aspiring towards bigger and better even after they have found a property that comfortably accommodates their entire family. I personally don’t agree with this strategy, I think it’s better to live in a slightly less optimal house to make it more affordable to buy to let. The beauty of a buy to let is that someone pays the mortgage off for you. I see it is a way of saving using someone else’s money. I won’t even go into the fact that many people don’t understand how stock investing works nor do they want to get involved in it because the idea makes them feel uncomfotable. Property investment is not a sure fire winner, it does sometimes result in severe regret either because one ends up buying in the “wrong” area or finds that the property has structural issues that cannot be easily resolved or for some other reason. Despite this property will always be high up on my list of favourite investments because it offers access to leverage and to cash flow opportunities.  I'm really irked by the assumption that reduced payments are the only reason one would go for an interest-only mortgage. This seems to be the central assumption of every single article that I have found on the topic. With a standard fixed interest rate mortgage, fixed identical payments are made for the duration of the mortgage, call it 25-years and by the end of that term the mortgage has been entirely paid off such that the house is now fully owned by the person that took out the mortgage. With every payment that is made, part of the payment goes to interest and part of it goes towards chipping away at the borrowed money. To begin with most of the money paid goes towards the bank's interest and very little goes towards capital repayment and with every successive payment the interest portion falls whilst the repayment amount rises as in my diagram below (assumes a £250,000, 25-year mortgage with a fixed rate to term of 3.30%, payments are £1,225 per month). Simple.  With an interest-only mortgage every payment goes towards interest only so at the end of the term you still owe the full amount on the mortgage. Simple? Actually, it's not really as straight-forward as that. When I went mortgage shopping just over a year ago, the best interest rate I could find was on an interest-only mortgage. It just happened that this was the lowest interest rate I could find, however, note that it does not necessarily follow that interest-only mortgages have better rates than repayment-style mortgages. I wanted to pay as little interest as possible so I thought I would go for it provided my lender would allow capital repayments as well. It turned out that there were no restrictions on capital repayments and the mortgage was an "offset" mortgage as well. This means that if my mortgage balance is £100,000 but I have £10,000 sitting around in my current or savings account, I only pay interest on the £90,000 - win-win. I asked the lender what my payments would look like if this interest rate were applied to a standard repayment-style mortgage and decided to set up a standing order equivalent to the stated amount plus an extra £150. This meant that at the end of the first year I had paid almost £2,000 more than I would have had this been a standard mortgage. So, one can very well have an interest-only mortgage and treat it just like a normal mortgage, repaying some capital as and when it is affordable. A second advantage here is that if money is tight in any given month, I can reduce my mortgage payment to just the equivalent of the interest and not suffer any consequences such as a mark on my credit record or in the worst scenario, repossession. I believe I went the smart way about it (please tell me if I'm wrong), however, I do know several people who have gone interest-only and have never made a capital repayment since they got it. Not even once. All extra cash has been spent on fun and frivolities. This could either be because they are not aware of the fact that you can make overpayments on an interest-only mortgage or because they are not adequately thinking about the future. Owning my own home is my dream and the dream of many other people. Unfortunately, many still think of their home as entirely theirs even where the bank owns the largest holding. If you haven't thought about how you can use interest-only mortgages to your own advantage, I hope the above helps to nudge you forward in the right direction.

"I love this woman, I wish there were more like her on TV, the rest of them are just too frivolous!" my boyfriend said excitedly halfway through Episode 3 of Channel 4's brand new series Superscrimpers: Waste Not Want Not. I knew exactly what he meant, when he'd reminded me she'd be on later that evening I'd widened my eyes and inhaled deeply like a five year old girl presented with a bar of candy because the show is a real treat.

There are three aspects to the show: 1) Mrs Moneypenny shows a family with a financial goal how they can achieve it, 2) Mrs Moneypenny and her army of Superscrimpers shows the rest of us how we can do better and 3) Merryn Somerset Webb gives us a few investment tips. Episodes 1 and 2 showed families that were overspending by a large margin despite a healthy disposable income. I was frankly a little dismayed at how people can have such poor control over their finances, but hey, who am I to judge? Episode 3, on the other hand, showed a family failing to save enough for a deposit to buy their own house, again because they couldn't identify areas where they could cut back or indeed how they could juice up household income. A colleague watched the show for the first time last night (I've been begging him to) and thought it was pointless because everything was so obvious. However, is it? Common sense is not common to everyone (I paraphrase the French philosopher, Voltaire). We work in finance and as such, relative to the average person, spend a disproportionate amount of time thinking about money matters and so should be better placed to manage our money (I'd hope). Indeed,most of the worst money-handlers I know work in finance. If you grew up switching off lights, turning the tap off when you're brushing your teeth, switching appliances off at the mains when you're not using them - well then it becomes second nature to you. If not, having to change old habits is a real chore, you're ever tempted to revert to old ways. The show has actually come at a very opportune time. The boyfriend and I have just recently come to the end of our first year of cohabiting and have been assessing our spending habits. It would have been very easy to slip into year two without stopping to do this evaluation but we did, and in the process discovered our electricity supplier had increased our monthly direct debit without informing us, all our insurers (home emergency and buildings insurance) were no longer the most competitive and we actually decided that some of the things that we look upon as base necessities should now be looked upon as treats. Chief amongst the things that have moved into the "treat" pile for me is lunch: I now take my own lunch into work. I am allowed to buy lunch say once a week but I'm now in week 6 of this challenge and will be buying lunch for the very first time on Friday. I thought the whole lunch thing would be an insurmountable challenge because I've tried it before and it didn't work but on all the days I would have failed (pretty much all of this week) the boyfriend's been there for me. Two weeks ago we stepped up our efforts by buying an electricity monitor and it has completely changed some of the things we do. It's straightforward to use, once set up it tells you how much electricity the house is currently using; you can then go around the housing switching appliances on and off to see how the energy consumption changes. The power shower completely shocked us - from a base of about 200kWh we were suddenly on 9,500kWh. To put that in money terms, we moved from using £20 per month to £900 per month in electricity usage just by switching the power shower on - given we both have two showers a day, it then became obvious why our energy bill had gone up since we'd moved to this house. Needless to say, that morning's shower was the last power shower I have had since, we now use the shower that's on our bath and frankly, I prefer it because I can get right in without waiting for the skin-scalding hot shot and skin-curdling cold shot that precedes every power shower. I hope all of the Superscrimping tips will be compiled into an e-book because some of them are priceless. The best one so far involves placing stockings in the freezer before their first worn to stop ladders forming - hello? Why did I not know about this before, I'll save loads of time and money with that one tip alone. Yvonne is my favorite Superscrimper, she's really quite adorable, but she is so hardcore I don't think I could ever implement any of her tips - she cuts collars off her hubby's shirts when they're fully worn and sews them back on in reverse to double their life span. Saving money is good but when you work 12 to 14 hour days, saving time takes precedence. There is a more subtle lesson to be learnt from Superscrimpers. The growth of the internet in collaboration with cheap and easy-to-obtain credit has made it so easy for people to spend money they simply don't have. I for one find it difficult to manage a credit card so although I can rack up airmiles and dozens of other benefits with it, I find myself spending more so I simply don't use one. Can Brits spend more wisely? Absolutely: as the chart below shows credit card debt jumped up by almost 500% from Jan-94 to its peak in Jan-10 so there's lots of room for superscrimping to reduce this debt mountain. As for me, there are 30 minutes in the week when my boyfriend has only got eyes for Mrs Moneypenny, but that's okay because I feel the same!

|

By Heather

|

RSS Feed

RSS Feed

Heather Katsonga-Woodward, a massive personal finance fanatic.

** All views expressed are my own and not those of any employer, past or present. ** Please get professional advice before re-arranging your personal finances.